Investors rode the wave of strong equity returns in 2021. While public equity fueled impressive investment returns, private equity and venture capital performance took portfolios to the next level. A few phrases can sum up the private capital trends in 2021: record-setting activity, eye-popping returns, and mega fund raises.

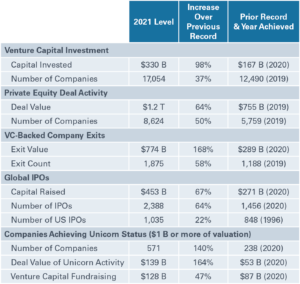

2021 Top Private Capital Records

2021: A RECORD-SETTING YEAR

The private markets ecosystem set several records in 2021. VC-backed companies raised $330 billion, nearly double the previous year’s record. All types of companies— from those seeking their first round of institutional financing to the ones participating in mega-rounds (greater than $100 million in financing)—benefited as a result. U.S. private equity clocked over $1.2 trillion in deal value, a hefty 64% increase over the previous record set in 2019.

Several factors contributed to the robust deal activity: the COVID-induced slowdown in the first half of 2020 pushed deals out to the third quarter of 2020 and into 2021, while also compelling struggling small business owners to sell. Cheap financing was broadly available, and entrepreneurs took advantage of a healthy ecosystem around company formation and innovation. Finally, potential tax hikes motivated sellers in advance of anticipated increases.

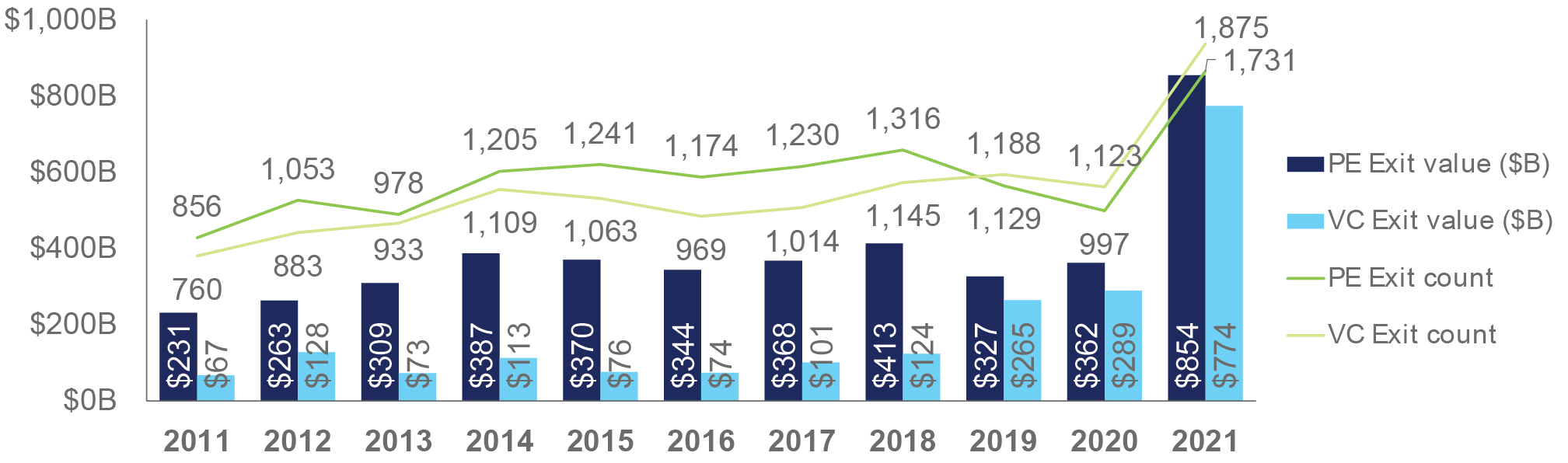

The exit side of the private company equation also set records. Venture capital-backed companies garnered $774 billion in exit valuation, predominantly through public market initial public offerings (IPOs) or reverse mergers into special purpose acquisition companies (SPACs), options also used by private equity-sponsored companies. In all, over 2,000 companies went public globally, with over 1,000 of them hailing from the U.S. The robust IPO market over the last few years was a welcome development for venture general partners that had carried companies longer and grown them into seasoned and revenue-generating companies, sometimes over a decade-long time period. Some firms also sold strategically to cash-rich companies, another popular exit option.

Private Equity and VC Exits

VALUATIONS

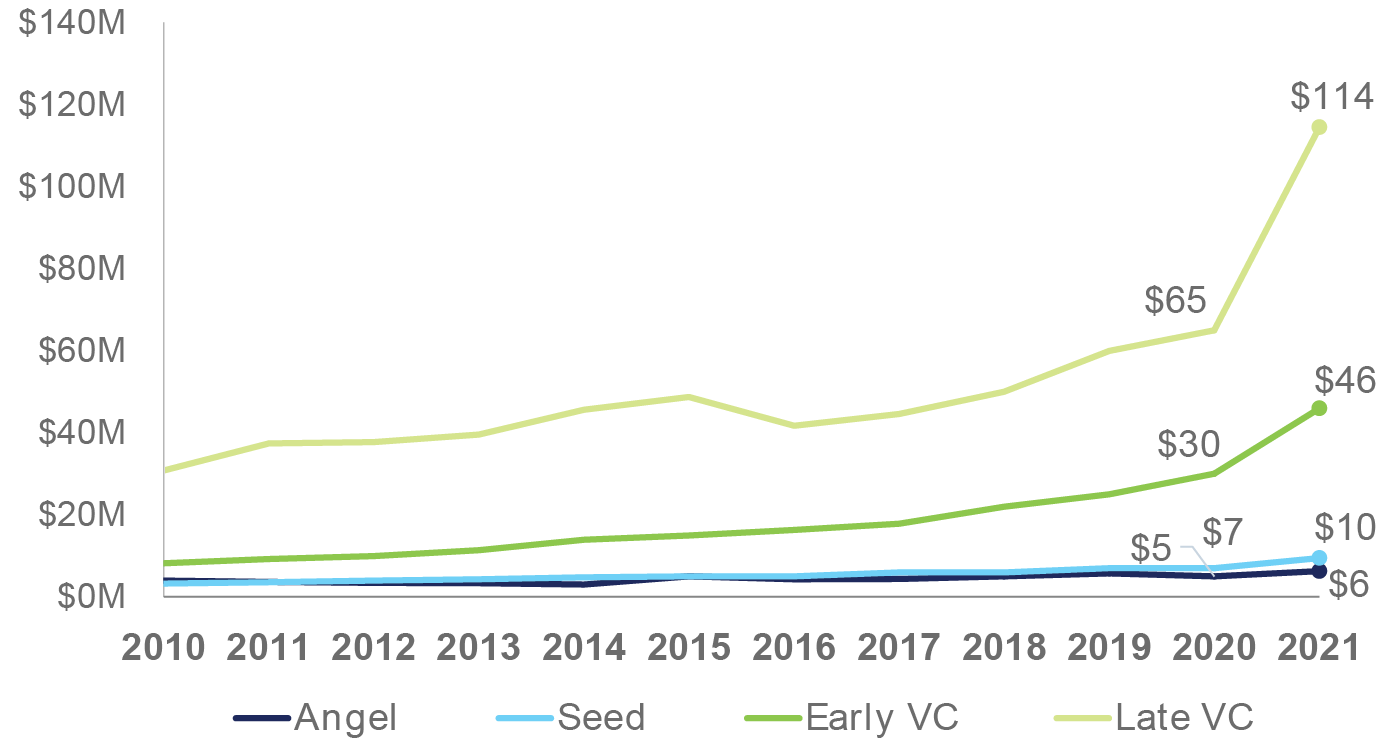

Robust deal activity not only helped exit valuations, but also positively impacted carrying values of funds’ holdings. The largest expansion of valuations was seen in the venture market, where pre-money valuations of VC deals expanded during the year. This was especially prevalent in late-stage deals, where a host of non-traditional investors participated in pre-exit activity.

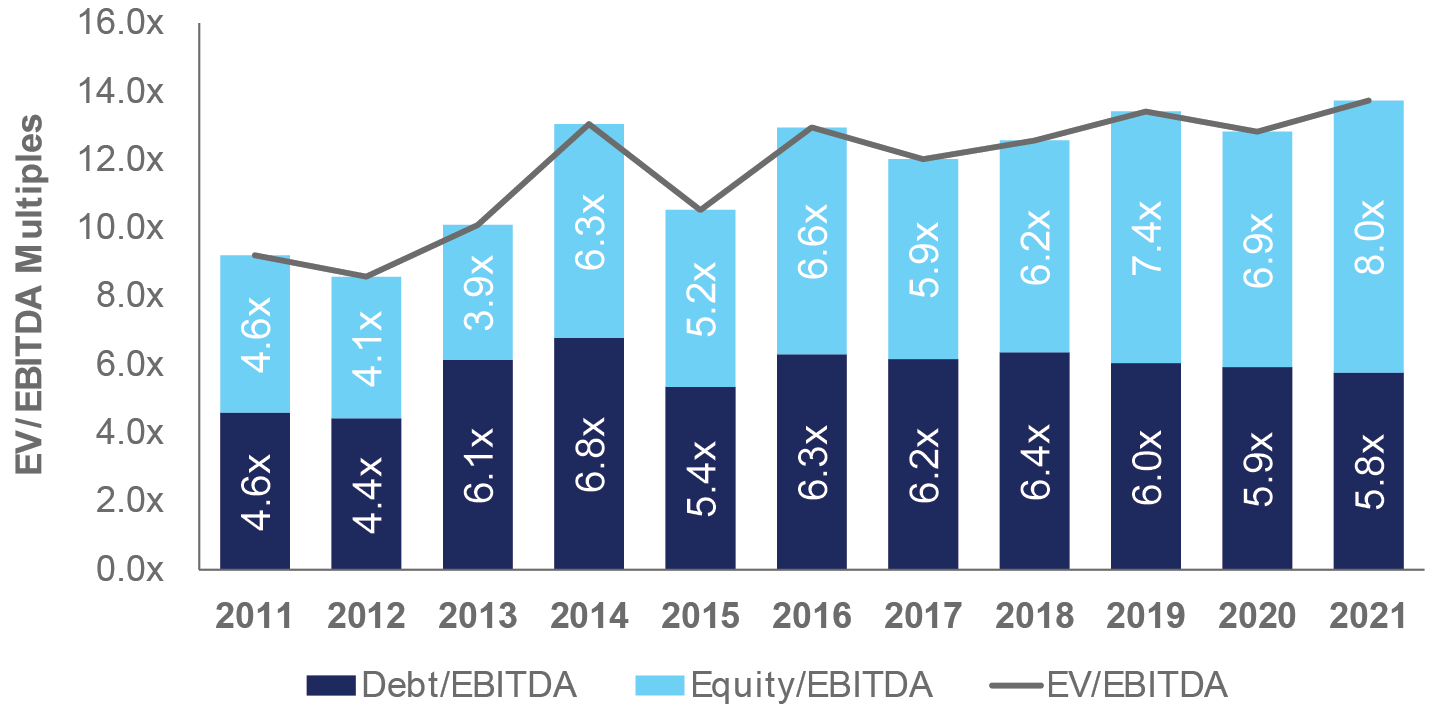

Buyout multiples also expanded, overtaking 2019 record-setting multiples after a slight compression in 2020.

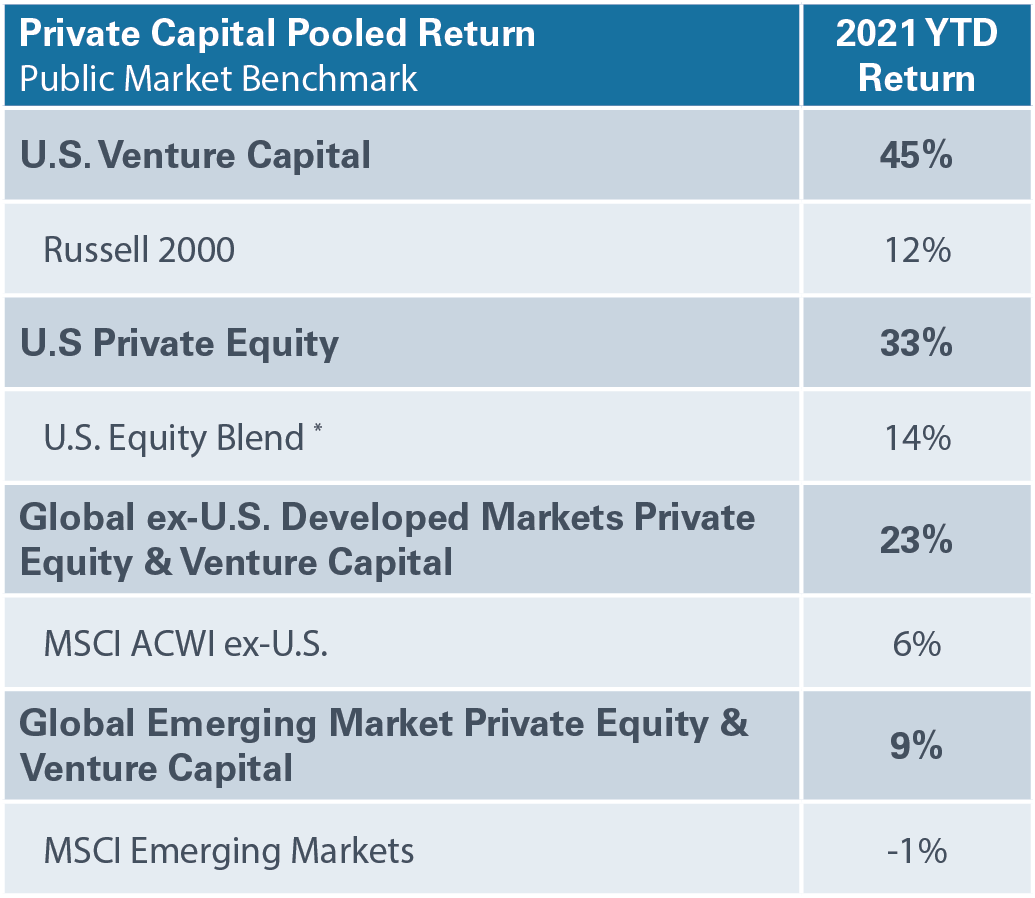

As a result, 2021 private equity returns led their public market equivalents by a wide margin. The following table presents the preliminary returns through September 30, 2021, the most recent available due to a lag in reporting.

Median Pre-Money Valuation

Median U.S. PE Multiples

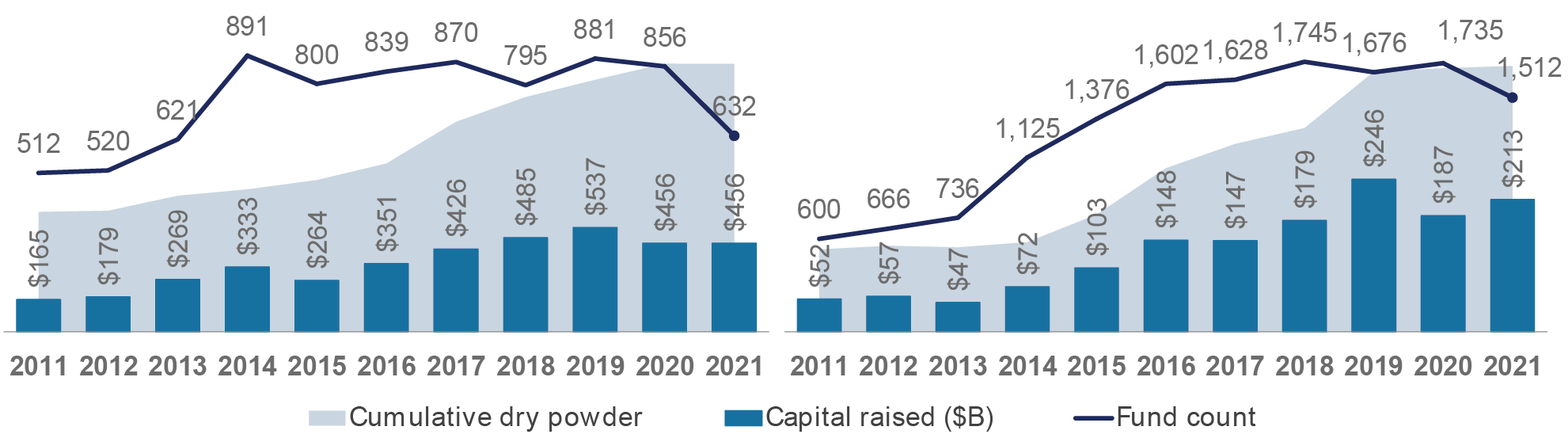

CAPITAL RAISE

Investors continue to allocate to private capital as public market prospects appear to be less fruitful. After record deal activity, general partners returned to the market quickly and, with higher targets, to secure more capital. According to Pitchbook, 31 mega funds (those seeking $5 billion or more) raised more than $329 billion in 2021. In late 2021 and early 2022, seven organizations were seeking or closed on funds raising $20 billion or more. Median private equity fund sizes are the largest they have been in a decade.

Venture capital fund raises were in record-breaking territory, gathering $128 billion in assets, a nearly 50% increase over the record set in 2020. Median and average fund sizes also jumped. The fresh capital adds to the capital overhang in both private equity and venture capital.

Private Capital Returns

Private Equity Fundraising

VC Fundraising

A STORM ON THE HORIZON?

Although there was a lot to celebrate with private capital funds, all was not rosy in the aftermarket. By the end of 2021, two-thirds of IPOs were trading below their IPO price, averaging a 9%-10% discount to their initial price.1

The sell-off in equity markets in early 2022 took that discount even wider. Formerly private technology companies, which have dominated the VC and IPO markets, followed the path of their public peers, which saw a peak-to-trough drawdown of 21.5% between November 19, 2021 and March 14, 2022. Technology companies have been under pressure since late summer last year, when Chinese technology companies came into the regulators’ crosshairs. Market turbulence continued as the global inflation characterization moved from transitory to sticky, prompting increasingly fervent discussion of rising interest rates, which can put pressure on valuations of growth companies. This concern has also pushed down pre-money VC valuations in early 2022.

Private equity investors also faced a conundrum driven by the category’s success in 2021. Many investors experienced a rapid rise in their private equity valuations, placing their allocations near or above their targets. With uncertainty around lagging valuations, unrealized gains and volatile public markets—a leading indicator of private market valuation activity—and target-hugging allocation levels, these investors will likely consider a slowdown in future commitments.

Some market followers are pointing to similarities in today’s venture market with the technology bubble that burst in 1999-2000 and asking if we are on the verge of a major contraction of venture value. Those that challenge that historical reference point to a different type of venture capital ecosystem today compared to two decades ago. Today’s ecosystem boasts an abundance of capital and talent, as well as entrepreneurs who are motivated to embrace risks to improve lives and tackle major societal challenges. This more optimistic view recognizes the valuation increases but believes innovation will continue through a supportive venture environment.

OUTLOOK FOR INVESTORS

NEPC continues to recommend private equity allocations as an important component of a diversified portfolio and anticipates that private companies will enjoy a premium over their public market brethren. However, it is also important to caution that we do not expect the meteoric rise of valuations that we have recently experienced, nor do we anticipate the record level of exits that private capital has enjoyed. Less support from monetary and fiscal policies has the potential to disrupt pricing and risk-taking in markets, and market fundamentals may reassert themselves over these external factors.

With that backdrop, private capital investors should keep a few things in mind:

- Be consistent. Continue to invest in a systematic way following an established pacing plan. Vintage-year diversification continues to be an important part of a private equity program. Now is not the time to skip vintages as one never knows what vintages will prevail in these long-life assets.

- Quality matters. This is especially true in areas of frothy valuations such as late-stage venture capital. Be sure that the managers utilized in these areas are the highest quality professionals who have dealt with a variety of market environments.

- Size down, but don’t skip. If your program’s private equity allocation is bumping up against policy limits due to the carrying value increases over the last few years, beware of passing on high-quality managers. Those highly coveted allocations may not be available in the future. Consider smaller allocations to those General Partners rather than skipping a vintage year.

- Diversify, diversify, diversify. Be cognizant of the sector allocations in your private portfolio. Strive for sector diversification.

As we head farther into 2022, it’s evident that market conditions have shifted significantly in only a few short months. Although we likely won’t experience a repeat of the record-setting activity and high valuations we saw in 2021, opportunities still exist for those who seek growth through consistency and carefully selected investments. Our best advice for investors is to remain diligent on selection, consistent with allocations, and aware of what is owned in the portfolio.

1 Wall Street Journal, December 29, 2021