Concerns that tax reform would discourage charitable donations are so far unfounded, according to the results of NEPC’s first quarter Endowments and Foundations survey.

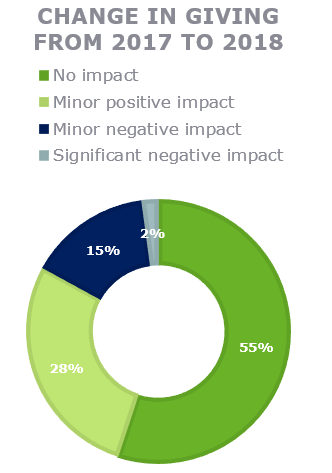

While the tax code—revamped in 2017—weakened the tax incentive to give, it is yet to dampen the spirit of charity. Of the survey respondents, 55% said they have not seen a decline in donations. The survey’s respondents comprised around 50 endowments and foundations whose assets under management range from $50 million to over $1 billion. In fact, 28% of the respondents reported an increase in giving. These findings echo the 1.6% increase in donations last year, according to the Fundraising Effectiveness Project.

Two giving strategies may be rising in popularity post-tax reform: gift bundling and donor-advised funds. Gift bundling, or bunching, refers to the practice of combining multiple years’ worth of gifts into a single year to itemize for the tax year. With

donor-advised funds, givers itemize a large contribution in one tax year, while allowing the donor to invest and distribute the funds in the future. Platforms for donor-advised fund accounts, for instance, Vanguard and Fidelity, have seen increases in new accounts and contributions. To this end, Vanguard Charitable saw a 22% jump in 2017 from a year earlier with nearly 3,000 new accounts; more than 2,300 of these accounts were established in the final days of 2017 on the back of the new tax bill that was passed on December 20, according to Vanguard data.

That said, endowments and foundations may not be out of the woods yet, with 36% of the survey respondents expressing concern that the tax reform may hinder future fundraising due to the higher standard deductions required by the new tax code.

The emergence of gift-bundling and donor-advised funds may signal a shift in giving, with high-level donors upstaging mid-level ones who may now lack the tax incentive to donate. Some worry that since 2018 is the first tax year following the reform, it is possible that endowments and foundations see a drop in future years that donors don’t bundle. There is also fear that donor-advised funds will lead to longer wait times for not-for-profit organizations to access their contributions, while encouraging donors to hoard assets for their heirs, thereby reducing current giving. To this end, non-profits may need to adjust their fundraising practices to offset the potential impact from the new tax code.

Still, 49% of NEPC’s survey respondents said that they would leave their fundraising strategies unchanged because they do not expect to be significantly affected by the tax reform. One expectation is that tax relief for the private sector will translate into greater capital investments and higher profits. In turn, the return on these investments will propel stocks higher, increasing potential fundraising opportunities for endowments and foundations.

Furthermore, tax policy is but one of many factors influencing charitable giving. In fact, research shows that GDP growth and S&P 500 returns are stronger predicters for charitable giving by individuals. By these measures, 2018 is a difficult year to read with the moderate increase in GDP offsetting the S&P 500’s poor performance. However, it may be too soon to tell. The upcoming tax years should reveal if non-profits have cause to worry—or if the reform is not so taxing after all.

If you would like to explore the impact of changing giving patterns on your institution, our total enterprise management (TEM) approach can help. Our model employs a holistic approach assessing your organizational needs. We can model customized giving scenarios in a variety of market environments. Our TEM study also incorporates an exhaustive review of spending guidelines, management costs and investment fees. We think about your portfolio in the context of total resources, including the balance between short-term operating needs and long-term growth objectives. Please contact your NEPC consultant to learn more about how we may help.