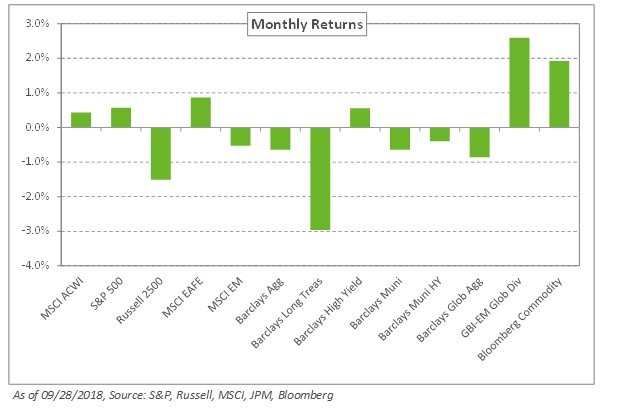

Strong economic data and positive sentiment pushed US stocks higher with the S&P 500 Index gaining 0.6% in September, bringing quarterly returns to 7.7%. Outside the US, Japan led the way with gains of 3% last month on the back of the country’s strongest job market in decades. In Europe, concerns around the United Kingdom and the European Union unable to reach a deal on Brexit at the upcoming October summit and fears of a debt crisis in Italy weighed on markets, with the MSCI Europe Index eking out a 0.4% monthly return. Meanwhile, emerging markets fell behind amid ongoing uncertainty around trade with the US and the Federal Reserve’s tightening monetary policy; the MSCI Emerging Markets Index declined 0.5%, with small-cap emerging markets faring worse with losses of 3.3%.

Still, it was not all bad news for emerging markets: fixed income rebounded after the recent sell-off with the JPM EMBI Global Diversified Index increasing 1.5% as spreads narrowed nearly 40 basis points during the month. Additionally, local debt, as measured by the JPM GBI-EM Global Diversified Index, rose 2.6% as dollar strength stalled and concerns related to Turkey’s currency stabilized following a central bank rate hike of 6.25%. In the US, the Fed raised rates for the third time this year to a range of 2.00% to 2.25%. Global yields continued to rise with the 10-year Treasury increasing 20 basis points to 3.06% and the 10-year German bund rising 14 basis points to 0.47%.

In real assets, WTI crude oil touched a four-year high of $76.41 per barrel—despite an increase in supply—ending September up 4.9%.

With the macroeconomic backdrop relatively unchanged, we maintain our recommendation of an overweight to emerging market equities, given their attractive valuations and fundamentals. Further, we encourage the addition of safe-haven fixed-income exposure as rates continue to rise.