University endowments breathed a sigh of relief in fiscal year 2023, as global investment markets bounced back from a gloomy 2022. Despite the good market news, however, many mega endowments1 posted results that lagged behind smaller institutions. This represented a significant reversal of fortune, as larger institutions have consistently outperformed their smaller counterparts over the past several years.

The key ingredient in this performance trend has been the role of private equity and venture capital in mega endowment portfolios. For multiple years, the largest institutions have benefitted from larger allocations to private investment opportunities. However, public markets raced ahead of private markets in 2023, adding value to the smaller institutions that tend to have more of their portfolios invested in them.

PUBLIC VS PRIVATE

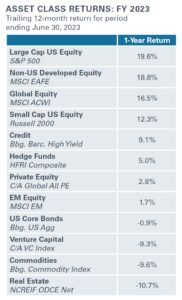

In the most recent fiscal year, private equity drastically underperformed public markets. At the start of the fiscal year, mega endowments—those with greater than $1 billion in assets under management, or AUM, as tracked by NEPC at the time of writing—had approximately 15% in venture capital and 18% in private equity. Endowments with $100 million to $250 million in AUM, where the median NACUBO respondent sits, had only 9% in private equity. Meanwhile, public U.S. equities—the top performing asset class—occupied less than 9% of the average mega endowments, and more than 28% of the average $100 million to $250 million endowments.

There were several factors that fueled public market outperformance. The overall economic backdrop in 2023 was significantly better than in 2022. Inflation receded, employment trends were positive, and corporate earnings improved after mid-year. Importantly, the Federal Reserve indicated plans to lower interest rates in 2024.

In addition, the release of Chat GPT in November 2022 drove an artificial intelligence-fueled rally. Initially, that rally was concentrated on the largest U.S. technology firms that have developed AI models, and mega-cap stocks that are benefiting from AI applications. But by year end, the rally had spread more broadly.

Meanwhile, private markets lagged. This isn’t a surprise – private equity valuations tend to be smoother than those of the public markets. They held their value better as public markets sank in 2022 and, subsequently, they did not participate fully on the upside in 2023. It is also true that rising interest rates this year were particularly problematic for highly-leveraged buyout and venture capital valuations. In other words, after multiple years of dramatic gains, private equity performance is returning to the mean.

The fixed-income market was a mixed bag in the public and private spaces. With the economy improving, credit opportunities posted strong gains, particularly in the high-yield space. However, interest rates rose over the course of the year, driving the fixed-income aggregate index to a slightly negative return.

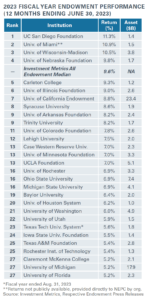

THE YEAR’S TOP PERFORMER – UC SAN DIEGO

The top mega endowment for fiscal 2023 was the UC San Diego Foundation. UC San Diego outperformed the median endowment and foundation as tracked by the Investment Metrics Universe; it is one of only four large endowments tracked by NEPC to do so.

Returns for the most recent year were driven by its decision to have a meaningfully higher allocation to public equity, particularly U.S. large-cap equity, than many of its large endowment peers. Public-market equity accounted for just under 60% of total portfolio assets, and it drove approximately 90% of the total returns for the year. As noted earlier, the average mega endowment held less than 9% of AUM in U.S. large cap.

The UC San Diego Foundation maintained a ~30% position in an S&P 500 Index Fund, which produced the strongest results of any major market segment. It gained additional U.S. large-cap exposure through other public equity investments. The remaining 40% of the portfolio performed modestly through the year, with excess performance in areas like fixed income and real estate.2

The UC San Diego Foundation maintained a ~30% position in an S&P 500 Index Fund, which produced the strongest results of any major market segment. It gained additional U.S. large-cap exposure through other public equity investments. The remaining 40% of the portfolio performed modestly through the year, with excess performance in areas like fixed income and real estate.2

LOOKING FORWARD

The past two years provide a stark reminder that markets tend to revert to the mean, and align with long-term trends, over time. This year’s trends were less an indictment of private equity and venture capital than an indication that their valuations had raced too far ahead of the public markets. Based on a variety of metrics, it also appears that the strong returns by public markets, particularly the U.S. Large Cap Equity segment, have pushed their valuations towards the higher end of their historical range.

Both areas produced strong returns during the ultra-low interest-rate environment of 2020-2022. But while the music is no longer as loud and returns may be muted for the next few years, we believe innovation will continue and those financing it will be rewarded – especially those who stick to their pacing and maintain discipline around strategy and vintage-year diversification.

This year’s trends also reinforce the importance of diversification in endowment portfolios. The ideal endowment portfolio targets some form of spending-plus-inflation return, with limited volatility. At NEPC, we continue to believe that diversification with a long-term vision are excellent tools to achieve those goals, even though performance of various asset classes may ebb and flow over time.

1 NEPC classifies a “Mega Endowment” as any endowment that meets or exceeds $1B in assets. Information for this report was gathered by analyzing publicly available data and public news releases that have been published prior to December 31, 2023. NEPC’s Mega Endowment list does not reflect data from institutions that do not provide readily available public returns, have not published their data prior to NEPC’s cutoff date, or do not meet or exceed the $1B threshold based on the 2022 NACUBO Report or prior versions of this list.