The COVID-19 pandemic, with its restrictions on travel and movement, and requirement of social distancing to contain the spread of the new virus, has upended life as we know it.

It has forced hedge fund managers to conduct work from the confines of their homes as offices become off limits, bringing to the surface concerns around their ability to successfully carry on their business operations remotely. Investors are especially worried about the disruption in services that hedge funds typically rely on for certain middle- and back-office functions, for instance, accounting, auditing and information technology. For service providers with a large part of their workforce offshore, lockdowns in those regions may make it difficult for them to perform their duties adequately and timely. To this end, the NEPC Operational Due Diligence Team carried out a brief survey to gauge the impact of the spread of the Coronavirus on the operations of the hedge fund managers on our focused placement list.

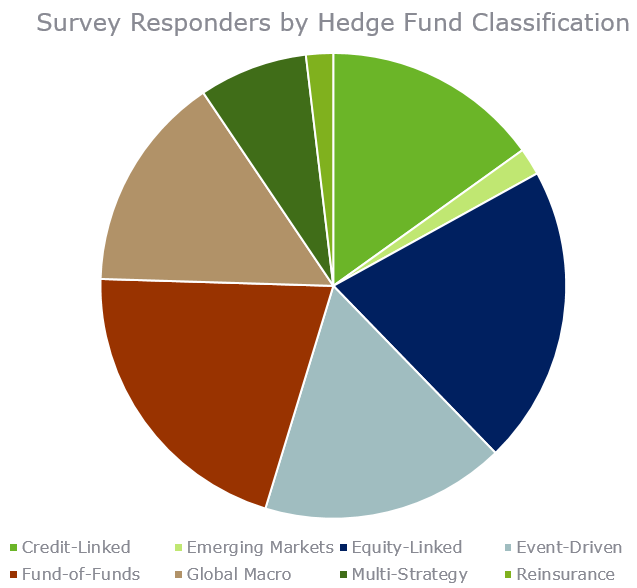

Our survey had 53 respondents. Here are the top findings:

- No fund managers reported any issues with transitioning all employees to a work-from-home model: Many respondents reported that they had moved fully to working from home. No respondent stated having any issues with this arrangement; many noticed an uptick in communication between employees and teams. Additionally, no fund manager conveyed any change in operational processes due to this new normal.

- No hedge fund managers reported any disruptions of service from key providers: Service providers such as administrators, auditors, prime brokers, and data and IT providers are continuing to provide crucial services to hedge funds. In addition, all hedge funds reported that they have had discussions with their key providers about their business continuity plans and are comfortable that service will continue uninterrupted despite the lockdowns that many are dealing with.

- Some fund managers noted adverse changes in liquidity: Credit-focused hedge funds described significant disruptions in their markets, and challenges in trading and obtaining financing through repurchase agreements with counterparties. On the other hand, long-short equity funds did not report any issues with liquidity or prime-brokerage financing.

- Some fund managers noted that they were close to setting off NAV triggers: triggers related to the net asset value are typically embedded in ISDA (International Swaps and Derivatives Association) agreements between the fund and the counterparty. They generally state that if the net asset value falls by a certain percentage within a month or quarter, the counterparty can terminate the trading relationship with the fund at the expense of the fund. During the steep selloff in equities in March, a few managers said that they were approaching their triggers. The subsequent rebound later that month helped give fund managers some breathing room.

Fund managers are currently reporting no significant issues or concerns, including with their key providers. That said, these findings may change over the near term given the ferocity with which COVID-19 is tearing apart economies. At NEPC, we continue to monitor the situation and will be sure report any significant developments.