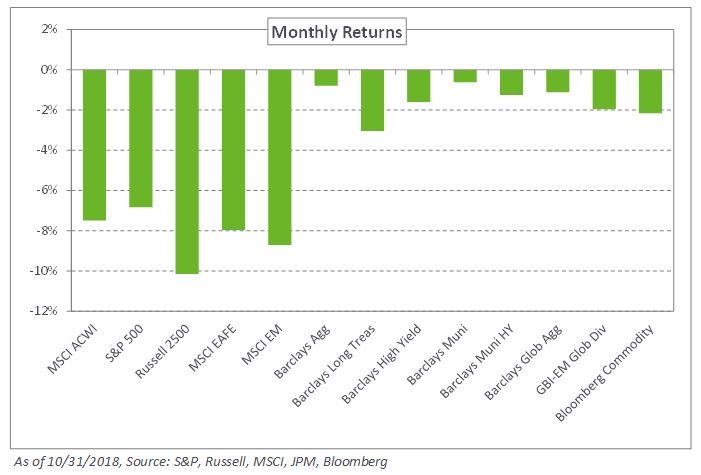

Volatility made a comeback in October as a wave of risk aversion washed over markets amid rising rates in the United States, growing concerns over slowing economic growth in China, and ongoing geopolitical tensions. Equities declined with international and emerging economies faring worse than US markets. The S&P 500 Index fell 6.8% even as the US unemployment rate declined to 3.7%, the lowest it has been in nearly 50 years. The MSCI EAFE Index lost 8%, while the MSCI Emerging Markets Index declined 8.7% last month.

Despite the risk-off sentiment, fixed income moved lower as well with US yields moving higher. The 10-year Treasury increased eight basis points to 3.14% and the 30-year Treasury increased 19 basis points – causing long-duration US assets to decline. The Barclays Long Treasury Index and Barclays Long Credit Index fell 3.0% and 3.6%, respectively. Local- and dollar-denominated emerging market bonds declined during the month. The JPM EMBI Global Diversified Index fell 2% as spreads increased 31 basis points in October.

In real assets, crude oil gave up some of its third-quarter gains, falling 10.8% last month. Despite this decline, spot WTI crude oil remains up 8.1% year-to-date. The Alerian MLP Index declined 8% in October as higher yields in the US render riskier assets relatively less attractive.

As rates edge higher, we encourage the addition of safe-haven fixed-income debt. We advise investors to trim any overweight positions in US stocks and consider reducing their overall exposure given current valuations and profit margins. Despite the continued pressure on emerging market assets, we still believe these economies are attractive investments and that the macro forces currently weighing on them will moderate in 2019. Finally, we remind investors to remain vigilant in the face of elevated volatility and to maintain a diversified risk-balanced portfolio to weather potential market sell-offs.