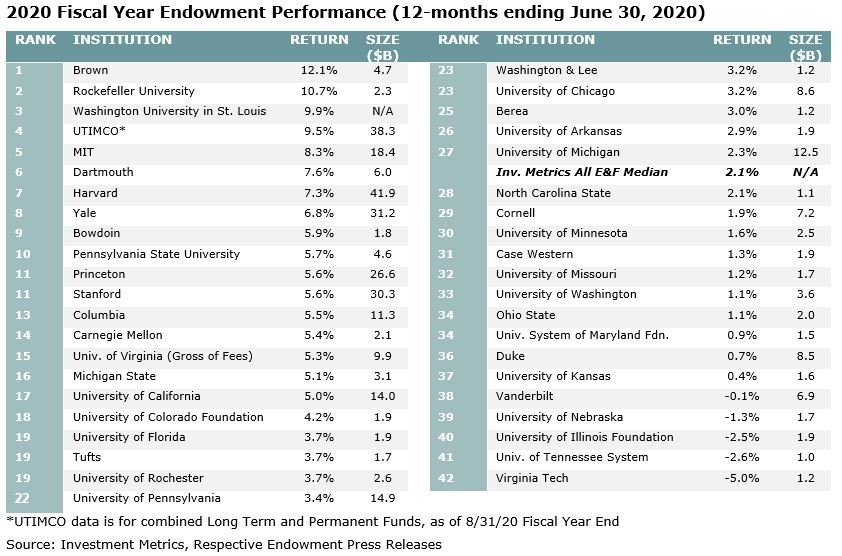

Keeping up with convention, the largest college and university endowments outperformed their smaller-sized peers in a year that was anything but conventional.

Amid a global pandemic and erratic markets, a number of top performing endowments saw strong performance thanks to their bias towards technology within both public and private markets, their ability to access capacity-constrained managers and to identify other top-performing strategies. While most endowments are united in their purpose of providing support to their institution in perpetuity, the largest endowments have a significantly different profile. The mega endowments tracked below, with an average value of $8.3 billion, will have different risk tolerances and resources compared to the average fund size of $136 million in the broad Investment Metrics Endowment and Foundation Universe.

As many major college and university endowments publish their financial results for the fiscal year ending June 30, 2020, median returns totaled 2.1% (net of fees), according to Investment Metrics, in line with the performance of the MSCI ACWI Index during the same period. Similar to earlier years, this lags the results of the larger-sized college and university endowments we track, which saw median returns of 3.7% (net of fees).

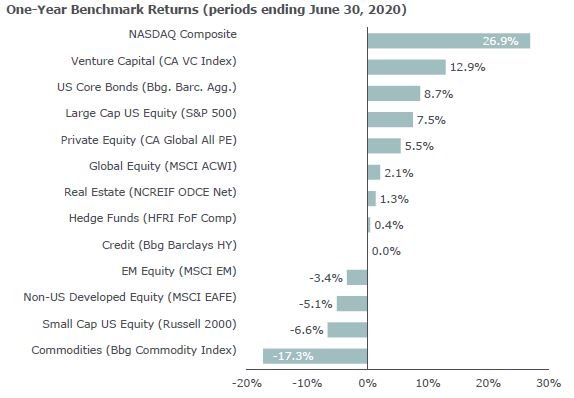

For the second straight year, Brown University’s endowment topped this exclusive list, with returns of 12.1%. Chief Investment Officer Jane Dietze attributes the gains to strong risk management and manager performance. In addition, the endowment has largely cut all fossil fuel-related investments; oil and other fossil fuels were among the worst-performing investments with spot WTI crude falling 30% during the fiscal year. Historically, Brown has had a high allocation to hedge-fund managers and, while we do not know the fund’s exact composition, an article1 in The Wall Street Journal highlighted Brown’s investments in three tech-focused hedge funds as helping drive returns. An overweight to technology would certainly help explain the fund’s return this past fiscal year; public technology companies were among the strongest performing asset classes in FY 2020 with gains of 26.9%, according to the NASDAQ Composite Index. Its robust return was well-timed as Brown increased its endowment’s distribution for one year to help cover its COVID-19-induced budgetary shortfall along with issuing new debt and reducing expenses.

Harvard University, the $41 billion heavyweight, staged a comeback of sorts. Chief Executive Narv Narvekar is starting to see results from the restructuring program he launched in 2016. The endowment’s public-equity holdings returned an impressive 12.2% for the fiscal year, besting the MSCI ACWI Index by 10 percentage points. While not accounting for all the public stocks it holds, Harvard’s 13F SEC filings similarly indicate a technology bias with significant holdings in information technology and healthcare. The fund’s sizable allocation to private equity also contributed to performance, with returns of 10.2%, higher than the 5.5% in gains posted by the C│A Global All PE Index. Harvard does not break out its private markets exposure; however, Mr. Narvekar indicated in his annual letter2 that Harvard has a lower allocation to venture capital compared to peers, and that the team is carefully considering the amount of risk taken in this area. All in, it appears Harvard benefited from technology and growth holdings over the past year and the investment team maintains a favorable view of the space.

Last year we theorized that large endowments were generally outperforming their smaller peers due to higher allocations to private markets. For FY 2020, we believe this remains a driving factor. At the start of this year, endowments with more than $1 billion in assets under management had a 9% allocation to venture capital and 13.6% to other private equity, significantly higher than the 2.2% and 6.2% allocations, respectively, for all endowments3. While venture capital produced some of the strongest returns, the mega endowments likely did face some headwinds by being underweight strong-performing large-cap US stocks and core bonds in favor of their traditional overweights to more modestly-performing buyouts and other traditional private equity investments.

However, the mega endowments continue to benefit from mature private-market programs that are out of the J-Curve, while other institutions may still be building towards strategic targets.

At NEPC, we continue to assess the trends of the largest and top-performing funds. In the past fiscal year, a tilt towards growth and access to top-tier managers have been major contributors of success for endowments. Technology and other high-growth companies have excelled over the last decade and even more so in the past 12 months. That said, we still believe that value stocks are an important part of a diversified portfolio and manager selection is key to strong returns. To benefit our clients, NEPC’s 58-person strong research team works tirelessly to identify and gain access to the best managers. To learn more about how we can help you build and assess your portfolio, please contact your NEPC consultant.