Executive Summary:

- The COVID-19 crisis has led to health systems’ operating portfolios and income statements coming under stress, raising concerns about their ability to continue to fund their investments in innovation.

- The response to the virus has accelerated the adoption of telemedicine and virtual care, highlighting the need to leverage and embrace new technologies.

- The approaches employed to drive innovation include direct investments in companies, co-investments, and investments in private equity / venture capital funds utilizing a General Partner as a strategic partner.

Each approach to innovation has its strengths and weaknesses which are explored in this paper, along with our thoughts on the keys to developing a successful program.

Interest in strategic investing has been on the rise going back to the middle of the last decade. In our December 2016 white paper Caution: Construction Ahead – Healthcare Organizations Use Private Equity to Support Innovation, we noted The Affordable Care Act spurred the move from a fee-for-service to a fee-for-value model. In this new world, strategic investing is viewed as a tool to drive innovation and to support objectives, including:

- New medical advances to improve patient outcomes;

- Improve the customer (patient) experience;

- Establish new tools to facilitate revenue management and expense control;

- Monetize intellectual capital;

- Boost investment returns to support concerns of contracting margins; and

- Apply new technologies.

We see strategic investments in different forms. Some of the largest organizations, particularly academic medical centers, focus on developing businesses around their own intellectual property. Certain organizations seek direct investment opportunities in individual companies while others gain access to promising companies and technology through investments in private equity or venture capital funds. It is not uncommon for healthcare systems to pursue more than one of these approaches as part of their innovation program.

To help assess strategic investing in a post COVID-19 world, we divided this paper into four sections. The first section highlights how the response to this health crisis has adversely impacted the financial condition of healthcare systems. The next two sections assess the pros and cons of direct investments in companies compared to investing in a General Partner (“GP”) sponsored fund. In the final section, we will present our thoughts on implementing a strategic investment program.

An Altered Financial Landscape for Healthcare Systems

The financial impact of the virus has been dramatic as balance sheets and income statements have come under attack. The prolonged nature of this event will likely lead to knock-on effects for many strategic investment and innovation programs. In addition, there is a heightened awareness of possible similar situations in the future which will necessitate significant planning for health systems.

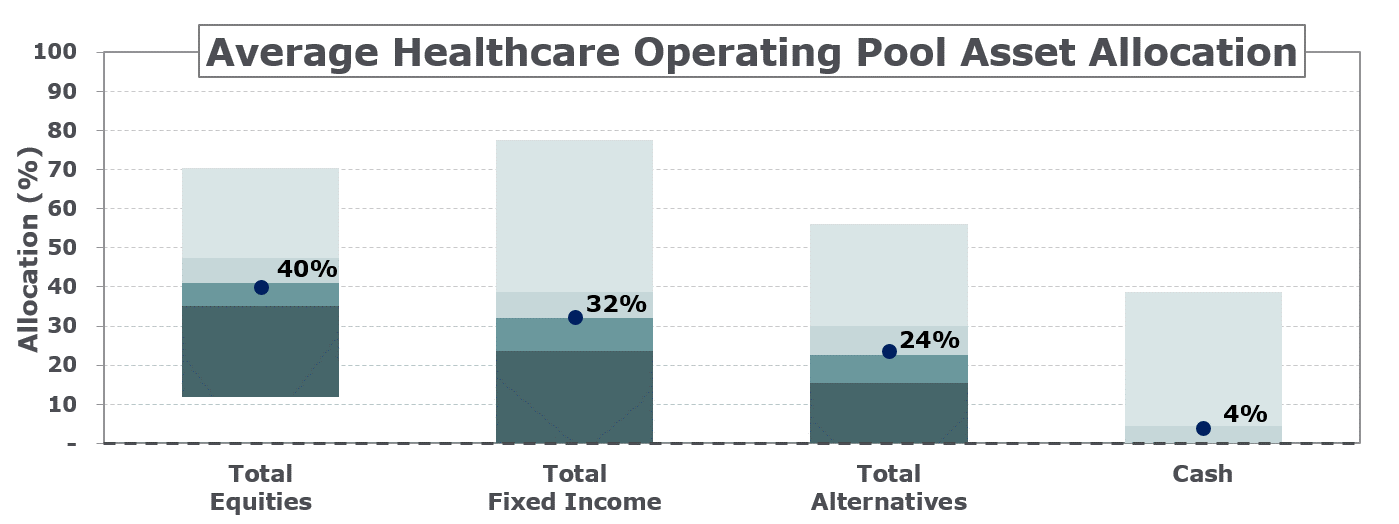

A non-profit healthcare system’s lack of opportunity to raise equity creates a reliance on operating cash flow / earnings and debt to fund the organization. Both operating portfolios and income statements are coming under stress. The table below highlights the average asset allocations of healthcare operating portfolios as of January 1, 2019. The data is from NEPC’s Annual Healthcare Operating Funds Survey which includes 68 organizations with investment assets ranging from under $250 million to over $2 billion.

Exhibit 1

Taking the average asset class allocations1 above and applying benchmark returns through March 31st shows that the average healthcare portfolio was down an estimated 11% in the first quarter. The results through May reduced the estimated market value decline for the year-to-date to 4%; however, operating losses will likely require many organizations to tap into their portfolios as restrictions on elective and non-essential services caused revenue to plummet. On May 13th, we published a poll of 51 healthcare organizations to examine the business impact and steps being taken to battle the pandemic, takeaways include:

- 61% of healthcare organizations have already furloughed staff, or plan to do so. The data also showed the larger organizations are handling the stress better as only a third of organizations with investment portfolios greater than $2 billion and/or a credit rating of AA had taken these actions.

- 43% have postponed/plan to postpone or suspend retirement contributions. Reducing employee compensation was also oft-cited to reduce costs.

- Costs are higher: Half of organizations polled experienced an increase in their daily cash burn of 10%, while 23% indicated a daily increase of more than 25%.

The challenges faced by the healthcare systems are being reported daily in the press.

- The health care industry experienced an estimated $500 billion reduction in revenue during the first quarter of 2020.i

- Phil Kaplan, a managing director at Hammond Hanlon Camp LLC, was quoted in HealthLeaders stating “as a result of the COVID-19 outbreak, provider organizations are likely facing challenges collecting revenues on time, which will create additional issues for paying for labor costs, medical supplies, and pharmaceuticals.”ii

- NPR reported on May 8th “Health care spending fell 18% in the first three months of the year. And 1.4 million health care workers lost their jobs in April.”iii

Balance sheet and operating pressures will also likely have implications on the strategic investments and innovation programs within healthcare systems. In a recent conversation with Harry Glorikian, General Partner at New Ventures Fund and the author of MoneyBall Medicine: Thriving in the New Data-Driven Healthcare Market, he made several observations. P&L’s are under pressure and CFO’s will be looking to cut cost for non-essential employees. Innovation programs can find funding when times are good, but when the environment turns, and capital becomes scarce, it is questionable whether most healthcare systems will be able to continue to fund their joint ventures and direct investments in companies.

Healthcare systems are facing a conundrum, they need innovation programs to generate efficiencies, improve patient care and to drive down cost, but how should they structure their strategic investment programs in the face of growing financial pressures? The following section will explore direct investments and investments in private equity/venture capital funds.

Direct Investments

Direct investments have a number of appealing features, including:

- The ability to target specific clinical needs;

- The flexibility to concentrate dollars into high conviction ideas;

- Greater control and transparency over investments;

- Enhanced ability to time entry and exit points for investment; and

- Potential fee savings over GP-led investments.

The last point is especially compelling, when the typical 1-2% and a 20% ‘carry’ private equity fee structure is applied along with other expenses, the total annual cost of these vehicles is estimated to be between 5%-and-7%. General Partners have historically generated gross returns of roughly 18% on buyout fundsiv. However, after accounting for fees, net returns earned by Limited Partners are estimated to be around 11% to 13%, leaving open the prospect of capturing part of the gross and net of fee return differential. Can this fee savings be realized in addition to the potential clinical benefits? The short answer is there is little evidence to show that direct investments outperform corresponding private equity fund benchmarks.

There is not a lot of data on the performance of direct investments, however, a comprehensive academic studyv was published in 2014. This study focused on the performance of direct investments from seven large institutions based in North America, Europe and Asia, including universities, corporate and government-affiliated entities.

Specifics regarding the study participants included:

- Average assets under management was $94 billion;

- Total alternatives totaled $21 billion;

- Average allocation to private equity was 15.8%;

- From 1991 to 2011, 390 transactions occurred; and

- Data on co-investments and solo deals originated and completed by Limited Partners.

The study showed that direct investments usually fall short of beating their private equity counterparts. Other highlights of the study included:

- Co-investments underperformed the investments in corresponding funds in which they co-invest; this underperformance is attributed to adverse deal selection.

- The risk of direct investments falling short of their private market counterparts is greatest when a unique skill set is required. This applies to venture capital where there is a premium placed on access to information.

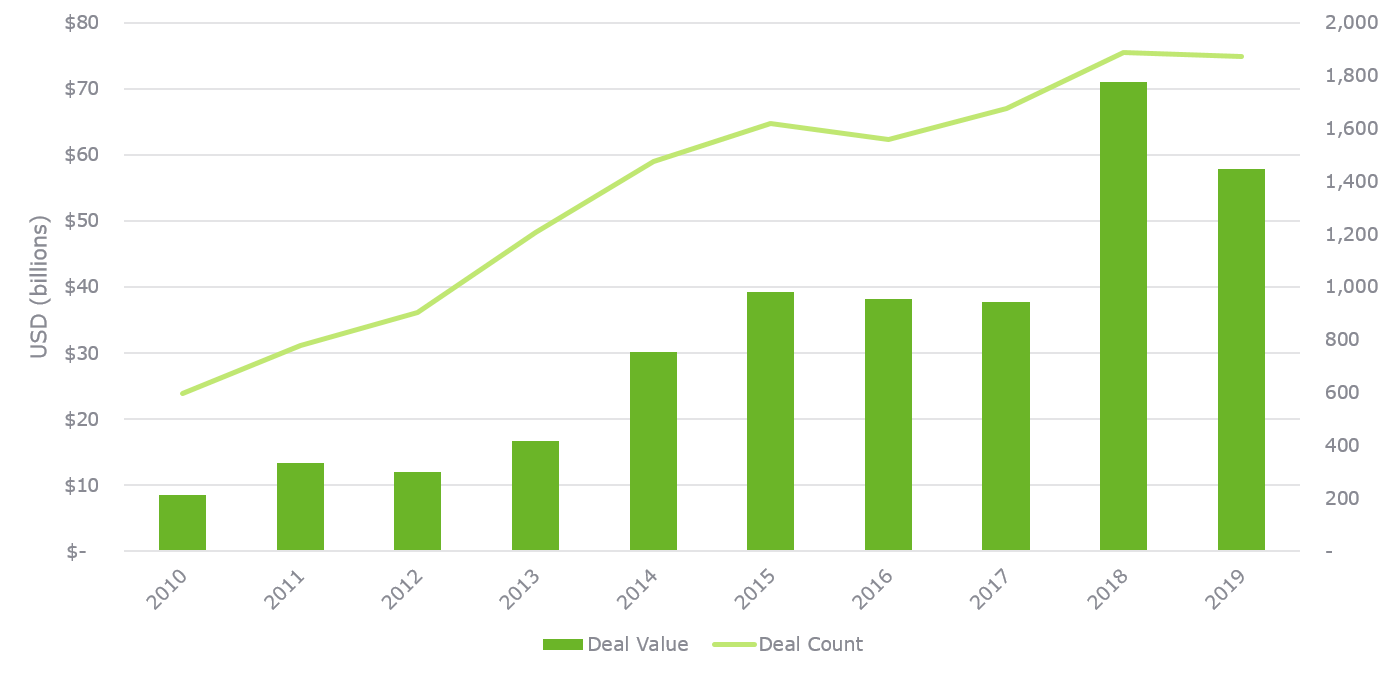

Another consideration impacting the return potential of direct investments is the amount of capital pursuing private companies. Corporations have increased their percentage of venture capital deal value from roughly 27% in 2008 to 46% in 2019.vi Venture capital investments made by corporations in 2019 are estimated at $57.9 billion (Exhibit 2).

Exhibit 2: US VC Deal Activity with Corp. Venture Capital Participation

Source: Q1 2020 PitchBook-NVCA Venture Monitor (Data as of December 31, 2019)

The impact of the virus will influence the amount of capital corporations will be investing in venture capital over the next several years, but corporations on a relative basis are likely to be in a better position to invest directly in companies than many healthcare systems.

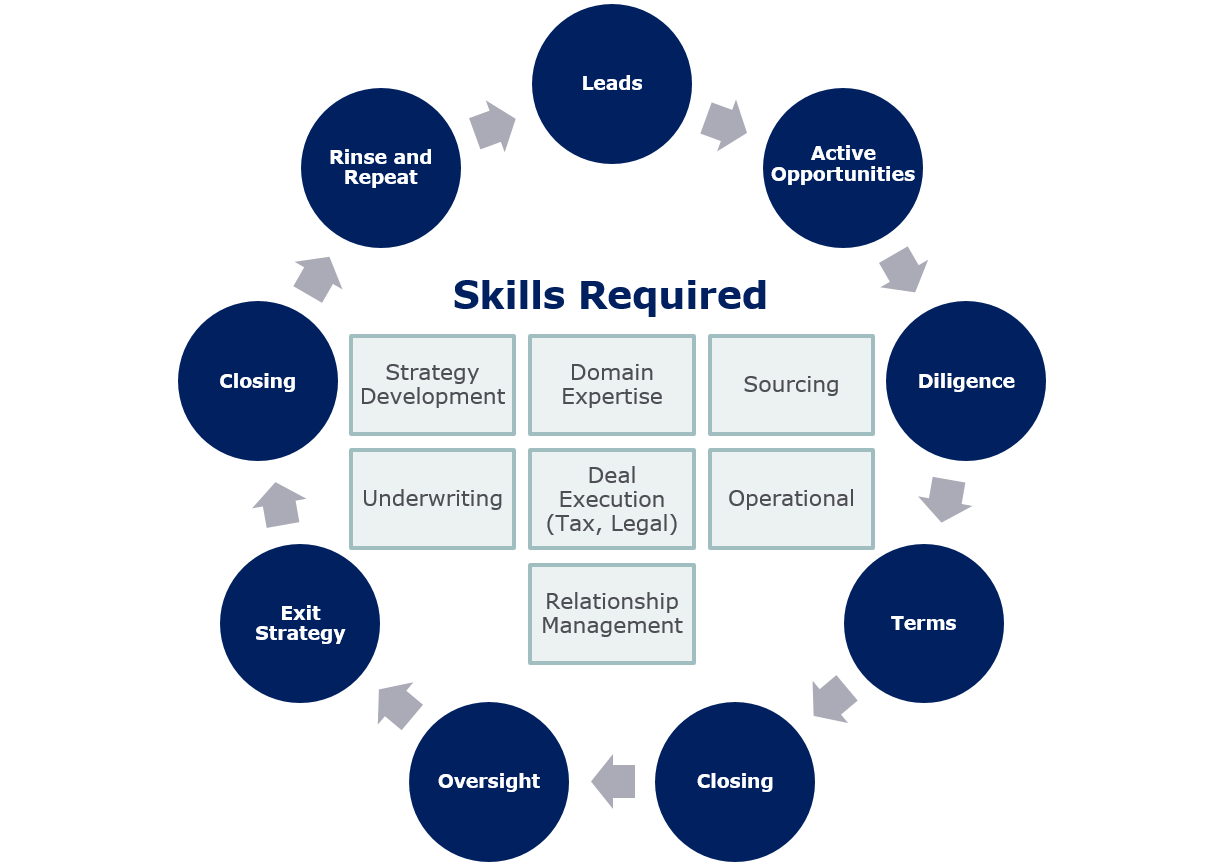

For healthcare systems to have a successful direct investment program, they should have the ability to address or overcome the information advantage held by General Partners. In addition, as highlighted in Exhibit 3 below, the skill set required to carry out direct investments is extensive, and the investment process requires numerous steps to convert a lead into a closed transaction, and the process repeats.

Exhibit 3: Direct Investment Cycle and Required Skills

What is not captured above is the advantage the healthcare systems have when evaluating a direct investment – after all, who better to know if a company has strategic benefit than the customer themselves? These investments can have a direct impact to the bottom line which can have far greater financial results than any single investment gain.

The highly regulated and fast-moving healthcare landscape can make these synergies difficult to adopt, resulting in high volatility. However, a well thought out strategy coupled with the proper diversification can result in innovation and in some cases financial success.

GP Led Strategic Investments

The universe of healthcare-focused private equity and venture funds is quite large. NEPC estimates this universe to be approximately 130 firms.2 The healthcare landscape consists of 80 venture firms, 30 growth equity firms, and 20 buyout firms.

It’s important to note that not all firms are created equal. NEPC has found through our research that many of these managers do not have appropriate risk-adjusted returns nor are they setup to manage strategic relationships with their Limited Partners. Those managers that do are often hard to access or have limited capacity for new relationships.

Advantages of investing with an experienced GP include:

- Access to all the investments underwritten by a GP (not just the fund you are invested in);

- Ability to partner with a GP given their desire to engage with HC systems;

- Ability to expand your peer network;

- Access to ideas/technology that may be advantageous to health system but was not known before;

- Ease of implementation; and

- Reduced financial risk.

There are also some challenges which include:

- Less ability to target specific clinical objectives;

- The GP’s ability and willingness to be a strategic partner; and

- Additional layer of coordination required to integrate the GPs with the HC system innovation team.

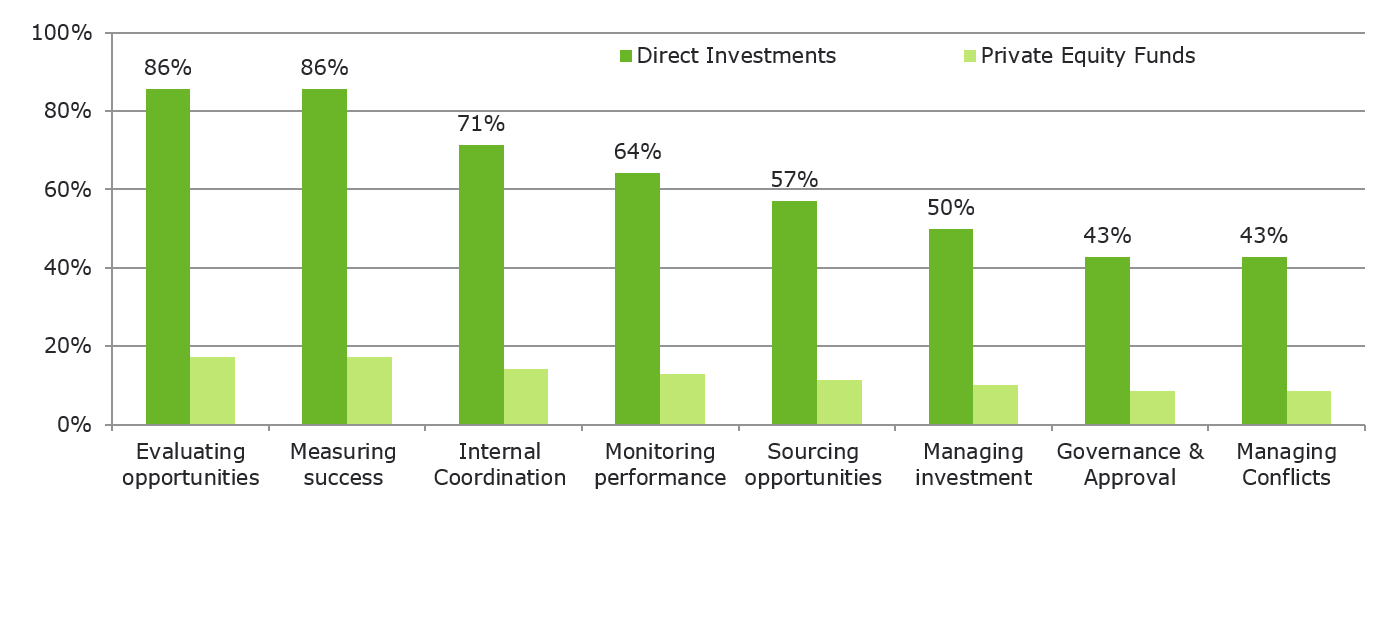

Evaluating direct investment vs. GP sponsored funds can be reviewed in a risk reward framework overlaid with an organization’s resources and skill set. In our 2018 paper The State of Strategic Investing in Healthcare Survey, we asked the roughly 20 respondents: Which tasks do healthcare organizations find challenging for both direct investments and private equity funds? The degree of difficulty associated with direct investments was much harder by a wide margin as shown below in Exhibit 4.

Exhibit 4: Which Tasks Do Healthcare Organizations Find Challenging

GP-sponsored investments are much simpler to manage from a financial perspective, and the downside risk is much less given each fund likely will have 10 or more investments. Realizing the potential clinical benefits tied to an investment may be harder since the company’s primary relationship is with the GP, so the organization may have less influence than in a direct investment.

Many healthcare organizations have experience investing in private equity funds but selecting a fund to be a strategic partner requires a different process. The GP’s ability to partner with a healthcare system and the breadth and scope of their network are quite often more important than identifying a manager who you believe will provide you with the highest return. Strategic investing is driven by access to ideas and networks that align with clinical objectives. The best manager in a specific space may not have the capabilities or the bandwidth to support a strategic partner. In our conversations with managers, they often cite they can handle only a few strategic relationships given their resources. That said, healthcare funds often desire having healthcare systems as Limited Partners as it increases their presence in the market.

As direct investing gains momentum GP’s have offered their Limited Partners the ability to invest alongside them, this is known as co-investing. This method of direct investing typically is done alongside a hired manager and is often offered at no fee or carry. GP’s are typically leading the deal but bring in their Limited Partners as strategic investors or financial sponsors. Co-investments seem like a natural first step when developing a direct-investment program. The advantage of co-investing is leveraging the underwriting work of the GP. The challenge is to avoid the potential anti-selection bias and the risks tied to too much capital being allocated to a specific deal or sector. These situations are typically associated with accelerated timelines and the co-investor is usually passive.

According to Pitchbook, in 2018, LP’s total co-investment deal value reached approximately $144 billion vs $4.1 billion in direct investmentsvii.

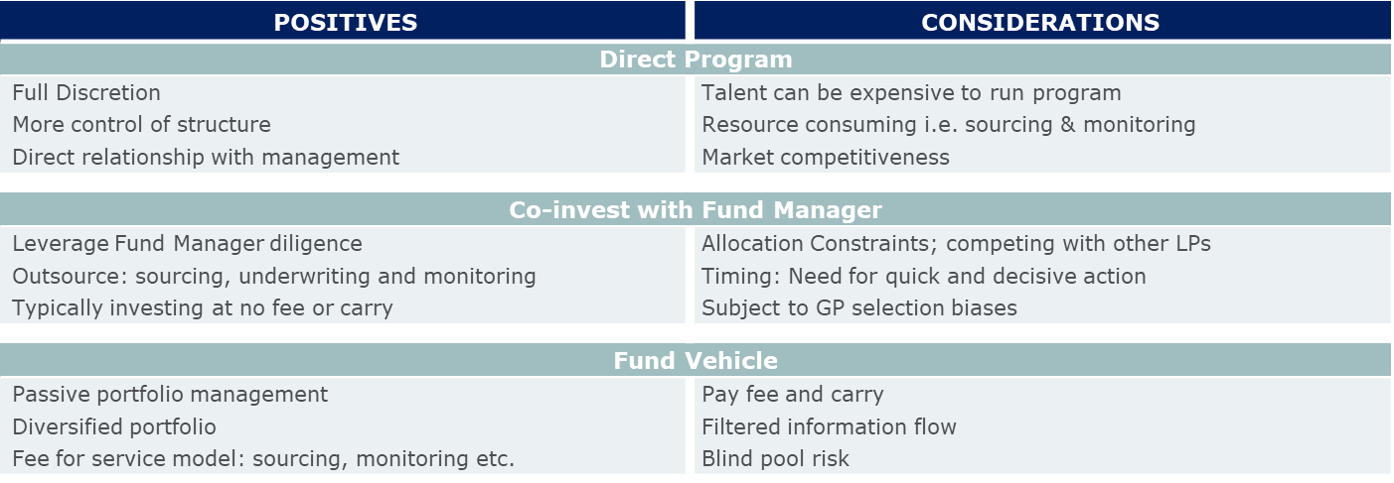

Exhibit 5 below highlights the benefits and considerations tied to a direct investment program, a co-investment strategy and investing with a GP in a fund. From the top of the table, Direct Program, and working down to Fund Vehicle, the level of discretion decreases. As that discretion decreases, third party fees will increase. However, the need for specialized talent will generally dissipate as portfolio construction and management functions, which are outlined in Exhibit 3, are outsourced. It is worth noting that scalability is easier as the portfolio moves downward on the table below, especially for immature portfolios. The table summarizes major points of distinction and is not meant to be a comprehensive list.

Exhibit 5

Strategy Development

When developing a strategy, we offer the following thoughts:

- Consider Different Investment Models: GP sponsored investments and direct investments are not mutually exclusive, with GP sponsored investments being a good way to start building a program as the skill set to be proficient at direct investments is extensive.

- Size Investments Appropriately: On direct investments, try to limit the amount of capital invested in a single company to manage the financial risk: this will place more emphasis on managing and focusing on the clinical benefits.

- Plan the Exit Before Investing: What is your plan if something goes wrong? The downside for a GP investment is to let the investment run-off over time. For a direct investment, the exit process may be long and difficult, ensure you are ready to deal with unfavorable outcomes.

- Stay Focused on your True Expertise: The academic study on the performance of direct investments noted the challenges tied to VC investments and those where the value of information is at a premium. Our survey also noted that most organizations are investing across multiple verticals. We would recommend identifying specific stages of investment to target and to narrow the verticals that are pursued. Does your organization have the culture and patience to oversee a venture portfolio?

- Develop a Sound Infrastructure: Based on our experience with clients, many are starting with small strategic investments and are “figuring it out” as they go along. Many organizations it appears would benefit from spending more time on initial governance and identifying resources and responsibilities. These include establishing and monitoring milestones and streamlining decision-making around the potential deployment of additional capital into a company when another round of financing is needed. At the time of the initial investment, it is important to know the capital needed to achieve the exit milestone as not participating in additional rounds of financing could lead to dilution of intended returns.

Which approach to strategic investing is best for a specific organization is influenced by numerous facts such as:

- Resources;

- Organizational stability;

- Clinical solutions being targeted;

- Role of innovation in managing financial results; and

- Organization’s culture.

The most significant benefits of direct investments (ability to target clinical objectives and fee savings) must be assessed relative to the downside risk (failed investments that detract value and distract management) and complexity of implementation. GP led investments can develop into partnerships which provide access to networks and ideas, albeit with less precision in targeting specific clinical objectives. Co-investments fall in between these two options. The good news is these different approaches are not mutually exclusive; for organizations that have been stretched thin by recent events, the GP led investments likely will offer the most efficient approach with the least downside risk.

Healthcare as an industry is filled with regulations and historically has changed slowly. The landscape is changing and given the massive size of the industry (~18% of GDP) it is now prone to be disrupted by outsiders as seen by large companies such as Apple, Google and CVS all making their presence felt within the industry. Are healthcare systems adapting fast enough to this changing environment? Harry Glorikian noted technology companies live in a world of disruption and “always have their heads up”. Having a GP as a strategic partner can provide not only access to companies that support clinical objectives, they support the building of networks and knowledge bases, and can help the healthcare system monitor trends and business risks so they avoid being on the wrong end of the disruption taking place in the industry today.

endnotes

iLayoffs and Losses: COVID-19 Leaves U.S. Hospitals in Financial Crisis

https://www.usnews.com/news/health-news/articles/2020-05-06/layoffs-and-lossescovid-19-leaves-us-hospitals-in-financial-crisis

iiCOVID-19 OUTBREAK THREATENS HEALTH SYSTEMS WITH NEW FINANCIAL CHALLENGES https://www.healthleadersmedia.com/finance/covid-19-outbreak-threatens-health-systems-new-financial-challenges

iiiAs Hospital Lose Revenue, More Than A Million Health Care Workers Lose Jobs https://www.npr.org/2020/05/08/852435761/as-hospitals-lose-revenue-thousands-of-health-care-workers-face-furloughs-layoff

iv“A Note on Direct Investing in Private Equity,” Ludovic Phalippou, Associate Professor of Finance, Said Business School, University of Oxford Tbd

v“The Disintermediation of Financial Markets: Direct Investing in Private Equity,” Lily Fang (INSEAD), Victoria Ivashina (Harvard University and NBER), Josh Lerner (Harvard University and NBER) (September 3, 2014)

vi“US VC Deal Activity with CVC Participation,” Pitchbook-NVCA Venture Monitor

https://pitchbook.com/news/reports/q1-2020-pitchbook-nvca-venture-monitor

viiThe Rise of Co-Investments, Megan Klassa, Research Associate

(https://www.marquetteassociates.com/wp-content/uploads/2019/09/The-Rise-of-Co-Investments.pdf).

About NEPC Healthcare

Employee-owned NEPC is one of the industry’s largest independent, full-service investment consulting firms, serving over 350 retainer clients with total assets over $1.1 trillion. Our Healthcare Practice Group provides investment advice to 43 clients with $98 billion in asset invested in operating portfolios, pension plans, endowments, self-insurance pools and defined contribution plans. NEPC services over 254 clients with over $67 billion in alternative assets supported by over 20 dedicated alternative assets research professionals.