Anticipating cash flows in and out of an investment program is a vital consideration in portfolio construction for high-net-worth individuals and their families. While the goal of some portfolios is to deplete over time, many investors aim to grow them to offset the effects of fees, taxes, inflation and spending.

In this paper, we discuss the numerous factors that go into ensuring the most optimal outcome is achieved when spending is a core element of an investment portfolio.

Step 1 – Understand Relevant Factors

To structure an investment portfolio keeping in mind a desired level of spending, the following must be reviewed to ensure predicted outcomes are achieved:

(i) Time Horizon

The duration of time a portfolio will need to support spending will likely impact the level of spending. In general, the longer the time horizon, the more prudent the spending level will need to be to remain sustainable.

(ii) Know Your Portfolio

To determine a sustainable level of spending, it is necessary to understand the mix of assets and the entities within the portfolio, and identify the source that will support the spending. Often, the total size of the portfolio may seem quite large relative to the desired level of spending. However, many wealthy families, as part of estate planning, create trusts to benefit multiple people and/or generations which limit access to the assets held within the trusts. Some trust structures contain the ability to grant access to currently-living generations, but this can reverse the benefits of the estate plan, especially if the intent is for these assets to be gifted to future generations.

(iii) Distribution Policy

Distribution policies of trusts vary with some allowing discretionary distributions, others mandating the distribution of trust income, and still others limiting distributions to health, education, maintenance and support. An individual family member may be the beneficiary of multiple trusts that have different distribution policies. Clearly identifying what spending can be pulled from specific trusts will help ensure there is no misunderstanding between beneficiaries and trustees.

Step 2 – Identify Goals

The next step is to identify and align the goals of the portfolio to the level of spending. This helps ensure that the spending is not hindering the portfolio’s ability to meet its objectives. For example, if the goal for the portfolio is to maintain a consistent level of purchasing power with the current asset base, the proposed investment structure would be different than an aspirational goal of leaving an increased level of wealth to heirs. Achieving the aspirational goal of wealth creation for inheritance may require either a reduction in spending or an increase in the risk profile of the investment portfolio. Exhibit 1 illustrates the need to match the risk profile to the spending amount to maintain purchasing power over time. Here, we show projected five-year market values for a portfolio with 20% equity and 80% fixed income, and an 80% equity (public and private) and 20% fixed income portfolio, along with two different spending levels of 2% and 4%.

Exhibit 1: Projected Portfolio Growth

Source: NEPC

Step 3 – Evaluate Risk

Once the portfolio’s goals are clearly outlined, it is important for an investor to be comfortable with the level of risk being incurred in order to achieve an expected return to support the desired spending. For example, a very aggressively-allocated portfolio may have an expected after-tax return that can support a higher level of spending over time; however, the investor may be uncomfortable with the associated volatility.

When evaluating risk tolerance, consider the flexibility to adjust spending during periods of extended market decline. By increasing the risk profile of the portfolio to stretch for return to support spending, one is also increasing the probability of a decline in value during a recessionary period. If the level or timing of spending cannot be adjusted, it may be necessary to sell assets at an inopportune time, thereby locking in losses and negatively impacting the portfolio’s ability to regain value as the markets recover.

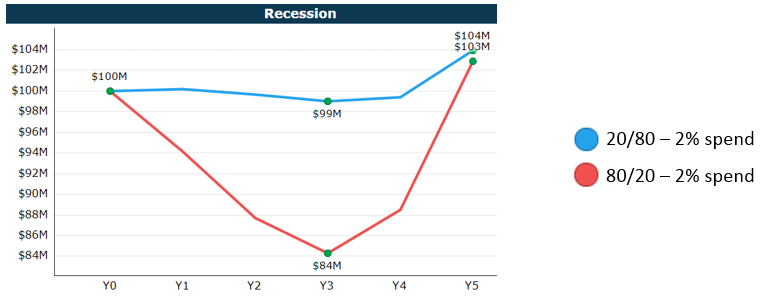

Exhibit 2 shows the potential market decline in a recessionary environment with comparisons to a portfolio with 20% equity and 80% fixed income, and one with 80% equity (public and private) and 20% fixed income, with a 2% spending level on both.

Exhibit 2: Recessionary Projected Portfolio Growth

Source: NEPC

If an investor is including illiquid investments to increase the expected return to support spending, a liquidity analysis should be undertaken to determine if the portfolio’s ability to meet its spending liabilities will be impaired in a recession.

Step 4 – Evaluate the Structure of Spending

After covering the potential portfolio risks, it is time for a deeper dive into the structure of the spending amount. The type of structure used depends on the investor’s needs and preferences. For instance, spending can be a set dollar amount per year, with or without an inflation adjustment. It can also be based on a percentage linked to rolling historical market values over a set time period, for instance, a three- or five-year rolling period, or can simply use the prior year’s market value. The spending structure should maximize the probability of meeting portfolio objectives without taking on unnecessary risks.

A percentage-based structure can be helpful to ensure the withdrawals reflect changes in market value. Thus, if the value of the portfolio decreases, a subsequent decrease in spending will occur. However, certain portfolios may require spending to be structured as a dollar-based amount. A spending amount that is less than the expected return on the portfolio increases the probability that the portfolio will be able to grow in value over time.

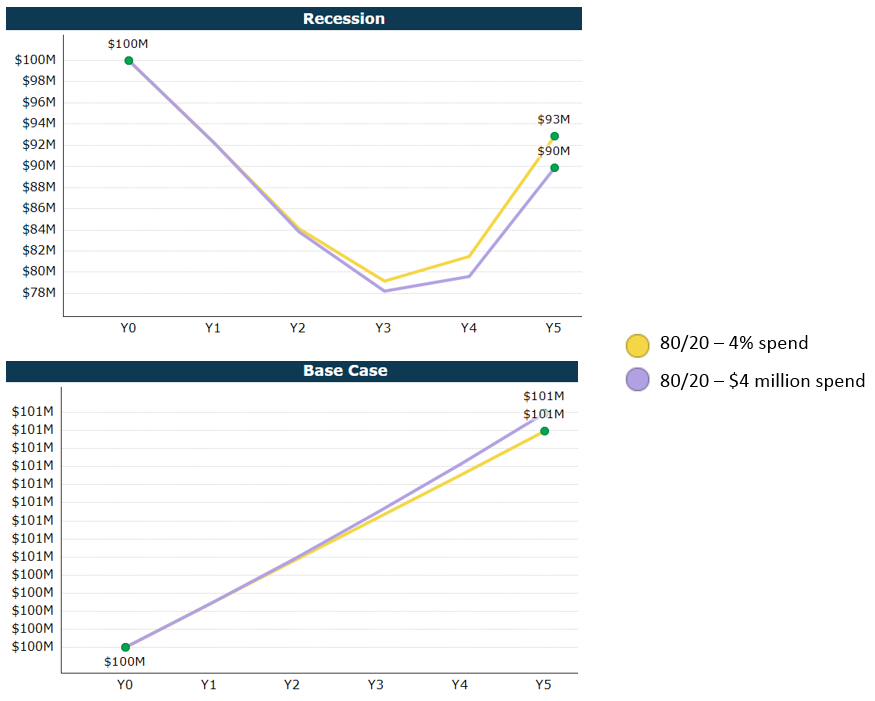

Exhibit 3 shows two charts projecting different dollar outcomes of spending structures in varying market environments. In a recessionary environment, a percentage-based spending amount projects a higher market value over a five-year period than a dollar-based figure. While in a base-case environment, the dollar-based spending amount projects a higher market value over a five-year period.

Exhibit 3: Percentage vs Dollar Spending Projected Portfolio Growth

Source: NEPC

When an aspect of the spending is related to gifts, we recommend reviewing assets with a low-cost basis to execute the gifting. We always suggest looking into tax-efficient ways to gift because benefiting from a tax deduction and removing lower-basis assets from the portfolio are a more optimal use of assets.

Step 5 – Ensure Ease of Administration

Finally, we must ensure the investing structure has been reviewed to allow for ease of execution. While certain investment programs are structured around a single legal entity, many portfolios come with structures with limitations on accessing capital, such as limited partnerships and family investment partnerships. Family partnerships allow investors to co-invest to meet investment minimums and obtain lower fees. While we support the use of these structures, we want to be aware of when limitations on accessing assets can interfere with providing liquidity for spending. With these structures, access is typically restricted to certain times a year, for instance, monthly, quarterly or annually, and must be planned to meet advance notification deadlines. We recommend reviewing liquidity regularly at the level of the individual legal entity as well as at the portfolio level to ensure adequate liquidity exists in the portfolio and these deadlines are not missed.

In addition, it is important to understand the tax implications and how gains/losses and income are allocated when co-investing with family members. Partial redemptions can trigger a taxable event and it is necessary to understand the allocation to avoid tax liabilities for non-redeeming partners.

Finally, we support maintaining a level of directly-owned assets (those not in a partnership structure) to provide ease of access to capital in instances when it is needed immediately.

Conclusion

The purpose of this paper is to ensure the most optimal outcome is achieved when spending is an essential part of an investment program. While numerous steps can be taken at the onset of implementation, changing market environments and the passage of time can have adverse or positive impacts to the structure. To this end, we recommend an annual review of the spending regime as it relates to an investor’s goals and structure.