Diversity has been an area of interest for endowments, foundations and nonprofits for decades. Promoting diversity has long been viewed as a way to dismantle structural inequities and generate opportunities for minorities, women and other underserved groups, goals that are often in alignment with these organizations’ missions.

This past year brought racial injustices into sharp focus, as the killing of George Floyd ignited widespread protests, laying bare the racial disparities exacerbated by COVID-19. The strong desire to redress these wrongs has fueled interest in diversity initiatives – in fact, it is one of the most frequent topics our clients raise.

In this series, we will lay out what it means to incorporate diversity, equity and inclusion (DEI) into your investment program, and explain why we believe it’s not only a valid strategy, but also a necessary one.

Is your investment program an appropriate place to pursue DEI goals? Until recently, few investment professionals had a confident answer to that question. However, that has changed dramatically. In this part of our two-part series, we will lay out why DEI initiatives are rapidly becoming a feature of investment programs.

Why Are Performance-Driven Investors so Focused on DEI?

“We found that companies with the most ethnically diverse executive teams are 33% more likely to outperform their peers on profitability.”– McKinsey research |

Women own 10% of all mutual fund firms; minorities own 9%. And yet, in both cases, the share of global assets under management held by these firms is less than 1% – in the case of minority firms, less than half a percent. What accounts for this gap?

According to a Knight Foundation/Bella Research report, whatever reasons might be involved, performance isn’t one of them. The gap persists, the report explains, “despite no difference in performance by standard measures of statistical confidence.” And this report is not the only one to reach that conclusion. For example, a study by NAIC supports the view that performance is not a valid reason to shy away from diverse-owned investment firms.

Other research has shown convincingly that, at a company level, having diversity of opinions and backgrounds is positively correlated with better decision-making and long-term results. As Deloitte noted in its research on the subject, “The business case for D&I initiatives is clear. More and more companies are realizing that diversity can drive innovation and increase productivity companywide.”

Tackling the Issue Head On

Foundations, endowments and nonprofits have pursued diversity programs in their investment programs for years – at NEPC, more than 40% of clients include diverse managers in their portfolio. But now that performance research has validated this mission-driven goal, the motivation to formalize and expand DEI programs has accelerated.

Groups like the Association of Black Foundation Executives are actively promoting diversity goals for investment pledges among its members. Universities and other large institutional investors are releasing data about the diversity of managers in their programs. Regulators (notably the SEC) are actively engaging in conversations with the industry about opportunities to improve access to (and disclosure of) data on diversity of ownership and leadership at asset management firms.

We are not surprised to see these efforts. In our view, incorporating diversity in your investment program is simply logical – excluding women- and minority-owned firms from consideration only limits our ability to meet the needs of our clients, and may restrict performance potential. Putting investment dollars in the hands of women and minority professionals is a powerful tool to uncover new opportunities and speed the closing of the asset gap.

DEI Dos

There are a few rules of thumb that we think help clients frame DEI in a constructive way:

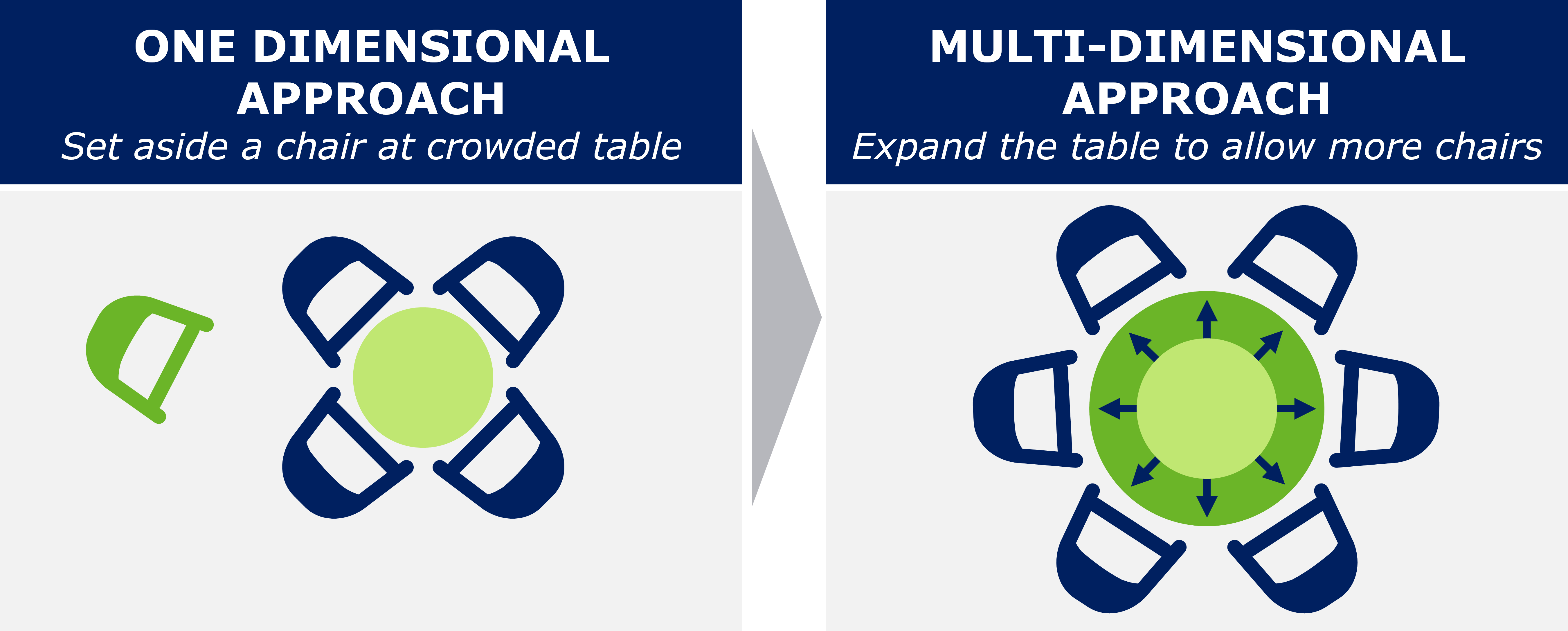

- Expand the table. Rather than simply adding a diverse manager to your existing roster – that is, setting aside a chair at a crowded table, it often makes sense to think more expansively. Consider the various roles that managers can have in your portfolio, and match diverse firms to specific, targeted goals.

- Think beyond diversity. Often, diversity is measured by the percentage of assets held with diverse-owned managers. But DEI also means equity and inclusion. Non-diverse firms can be fairly evaluated by the way they hire, promote, and make budgeting decisions to advance equity and inclusion in their practices.

- The S in ESG. Many endowments, foundations and nonprofits are embracing environmental, social and governance goals in their wider missions. For those organizations, DEI programs are often the best, most direct actions they can take to promote positive social outcomes.

- Evolve. Endowments, foundations, nonprofits, investment managers, and firms like NEPC are all trying to develop smarter, more effective approaches to DEI. Keeping your ear to the ground and adopting new ideas will be essential.

Next Up

In the second installment of this series, we’ll talk in detail about NEPC’s diversity toolkit and how it can drive positive DEI outcomes.