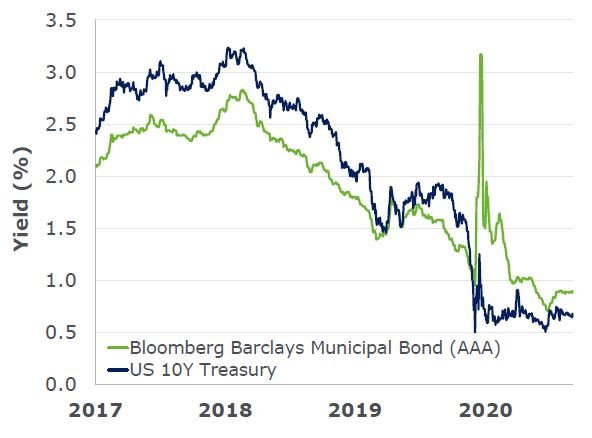

Yields for almost all high-quality bonds have fallen to record lows — US Treasuries, high quality municipals, high quality corporates, and other sovereign bonds currently all have yields under one percent. After taking inflation into account, the real return for many of these securities are in negative territory.

The low yields are pretty hard to get excited about and leave investors in a difficult situation. Should investors succumb to the new paradigm of accepting much lower yields, or should they reconstruct their portfolios in order to achieve a yield level that aligns closer to historical levels? Many investors are beginning to question whether it’s even worth continuing to invest assets in high quality fixed income.

Bonds have enjoyed an incredible multi-decade run, which has continued into this year.

The rise in large-cap growth stocks seems to be grabbing the headlines more recently, with an impressive year-to-date return of 24%1. We rarely heard about another phenomenal performer in 2020- long-term Treasury bonds. They are up a staggering 21% year-to-date — and that’s with a starting yield of 2.3% on January 2nd2.

While it’s unlikely that the magnitude and level of returns we’ve seen in quality bonds will persist, we do believe they continue to play an important role in portfolios.

With part of the value proposition for high-quality fixed income shifting, investors are taking a step back to reaffirm the purpose of holding quality bonds in a portfolio. An important element of this assessment is recalibrating to the current environment and resetting future expectations.

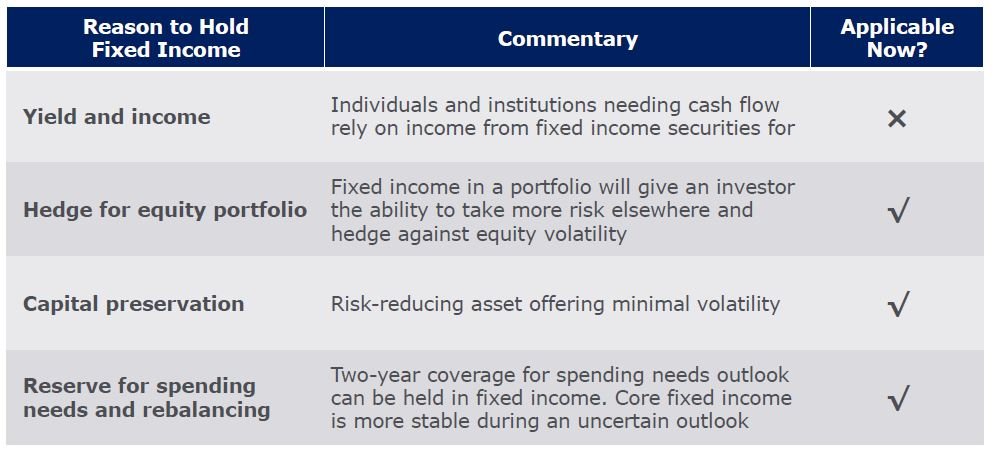

Below, we examine four reasons for holding fixed income and why such factors may or may not hold up in the current environment. Here’s why bonds should still hold a place in portfolios, even in today’s low-interest rate environment.

INCOME GENERATION

Historically, one benefit of holding bonds is that they’ve provided income. However, this is hardly the case anymore. Those seeking higher levels of income must look elsewhere, which isn’t an easy task. Attractive income-producing assets are hard to come by in the current environment.

Given current yield levels, investors may be tempted to take on more credit risk or illiquidity risk in search of higher levels of income. While allocations to these higher yielding areas can make sense for many investors and their objectives, they shouldn’t be viewed in the same lens as high-quality bonds. Still, we believe it pays to be patient and let opportunities arise with market conditions rather than moving out the risk spectrum to reach for yield.

While the prospects of attractive total returns and income in bonds have diminished, other benefits remain, providing additional sources of value to a portfolio.

FIXED INCOME CAN ACT AS A HEDGE

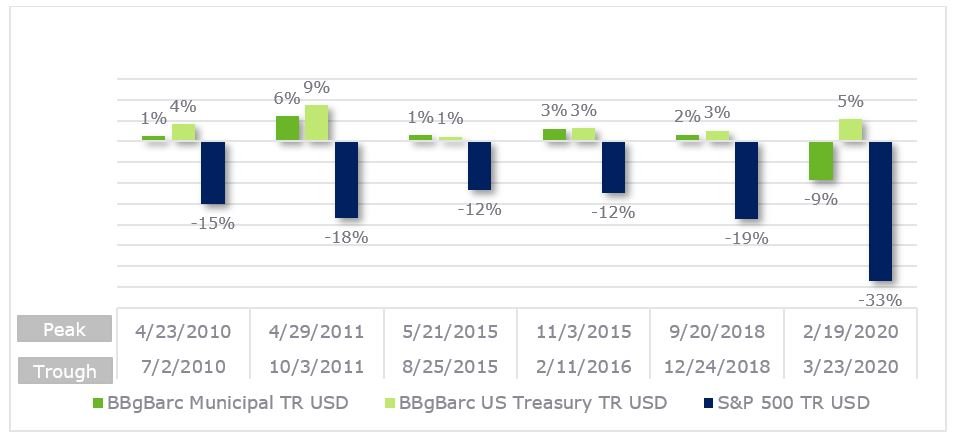

Quality bonds provide a hedge to equity volatility. Typically, bonds have a negative correlation with the equity markets. If there is a steep equity market sell-off, similar to what we saw earlier in 2020, bonds provide a much-needed ballast, increasing in value while most other assets decline. This is a valuable piece in the portfolio that pays dividends (no pun intended) when it’s needed the most.

By mitigating equity risk, bonds continue to play a crucial role in a portfolio.

Preserve Capital Without the Elevated Volatility

Investors seeking to shield a portion of their assets from volatility typically look for investments that offer capital preservation. While other asset classes, such as gold, can serve a similar role in portfolios, these types of assets tend to have more price volatility. Bonds help preserve capital with minimal volatility.

A Holding Location for Cash Needs and Rebalancing

Assets invested in fixed income can be used for spending purposes or as a source to rebalance your portfolio.

Given the current economic uncertainty, setting aside near-to-intermediate term spending needs to serve as an emergency fund is increasingly important. If equities decline and investors need to raise cash for expenses, locking in losses by selling equities that have decreased in value is the last thing a prudent investor would want to do.

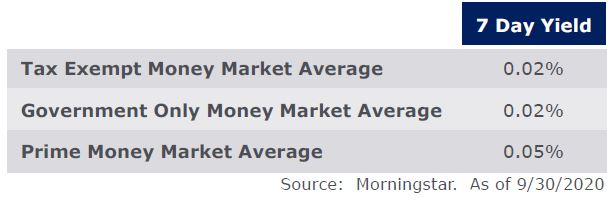

Instead, investors should consider holding a portion of reserve funds in fixed income. Even if potential future returns are minimal now, they will still generate some income. Alternatives, like bank accounts or money market funds, aren’t generating much of anything.

Fixed income can also be a good place to hold any “dry powder” for investment in the market. If equities decline to an attractive entry point, or an attractive investment opportunity appears, money invested in bonds can be used as a funding source to take advantage of these more compelling valuations if or when they arise.

VALUE REMAINS IN FIXED INCOME

Many investors are turning away from fixed income as record-low yields shrink the income these investments provide. But even in today’s low interest rate environment, high quality fixed income still serves an important role in the portfolio.

Holding fixed income today can provide an important hedge against stock market volatility, and also serve as a low-volatility holding for both cash needs and “dry powder” for future investment opportunities. Given the uncertainty of the economy and markets, a stable asset can serve as a ballast to the risk-taking elsewhere in the portfolio.