The recently-passed $1.9 trillion stimulus plan, the American Rescue Package Act (ARPA) of 2021, provides respite to single-employers struggling to keep up with contributions to their defined benefit plans.

The Act effectively lowers required contributions for corporate defined benefit plans by bolstering plan discount rates to address the historically low interest rates that have increased pension obligations. These changes will have an immediate impact, increasing plan funded status and decreasing minimum required plan contributions. However, this legislation does not affect the calculations for PBGC premiums or the accounting of corporate plans, leading to an ever widening disconnect between funding and economic liability measures. At NEPC, we believe this disconnect could complicate the management of these pension plans as plan sponsors toggle between the different ways of reporting plan funded status.

This most recent piece of legislation joins an alphabet soup of previous pension regulations. Market-based discount rates began with the PPA (Pension Protection Act) in 2006. In 2012, MAP-21 (Moving Ahead for Progress in the 21st Century Act) increased pension funding discount rates by including a corridor around a 25-year average of corporate bond yields. After being extended twice, these higher discount rates were slated to be phased out in 2021, in the midst of the economic fallout from the COVID-19 pandemic.

Now, the ARPA provisions not only increase the funding discount rates, but also extend the time period over which these rates will be used. In addition, the Act lengthens the payment period for unfunded liabilities to 15 years from seven. These changes may be retroactive to 2020 or delayed until 2022.

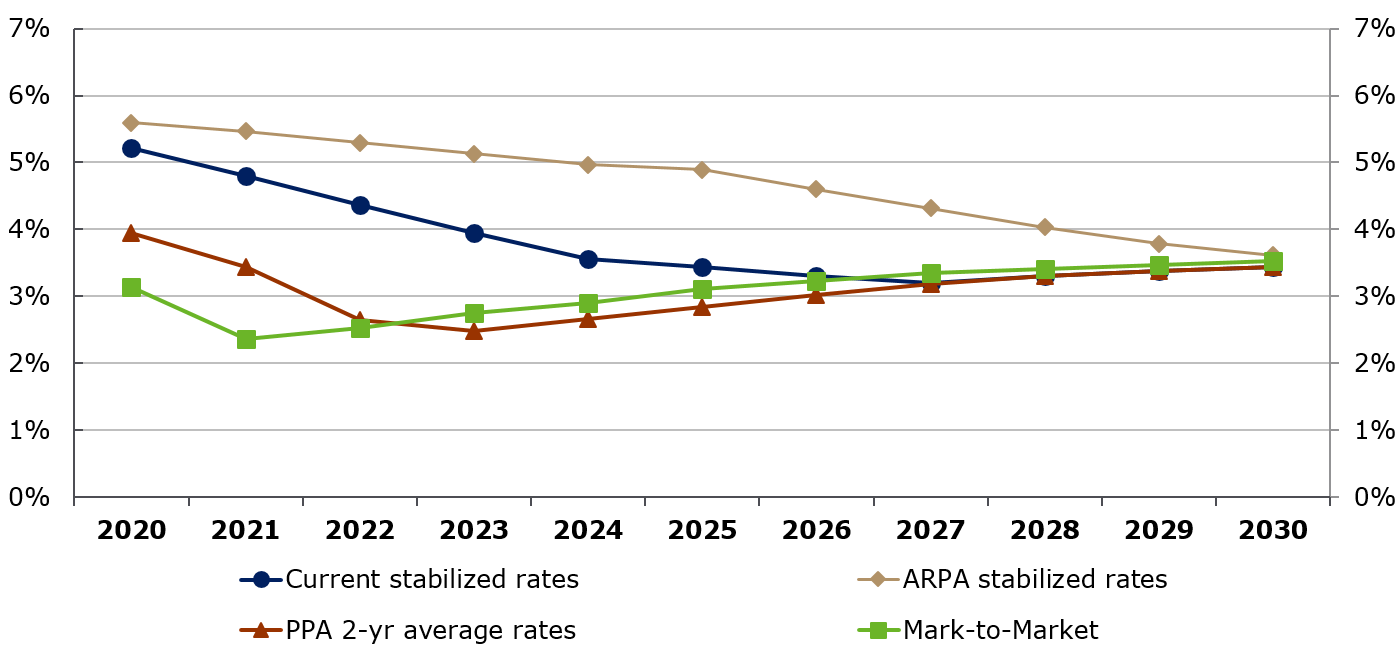

The long-term impact of discount rate changes in ARPA are projected below, based on the NEPC fixed-income model for future rates. The new discount rates (gold) are projected to be significantly higher than current stabilized rates (90% of 25-year average) (blue) and the current market rates (green). In 2021, the discount rates would be 0.7% higher based on a sample plan. Assuming a duration of 10 years, this would reduce liabilities by 7% for 2021, with this difference increasing through 2025. Note: the actual rates will vary based on each plan’s demographics and actuarial assumptions.

The red line represents the two-year average of corporate bond yields which is often used to determine PBGC variable premiums. The green line represents marked-to-market rates used for accounting liabilities and economic obligations, which form the basis for hedging plan assets and annuity purchase rates for plan terminations.

Source: NEPC

Sponsors impacted by the pandemic may benefit from lower contribution requirements, while others may continue to keep up with existing funding goals in order to become fully funded on an economic basis. Another consideration is the possibility of higher corporate tax rates in the near future, which would incentivize plan sponsors to delay plan contributions until those higher tax rates are in place. We remain focused on helping corporate pension clients manage these complex and intertwined aspects of their pension plans. Please reach out your NEPC consultant to learn more about the potential impact of this new legislation on your plan’s financial objectives.