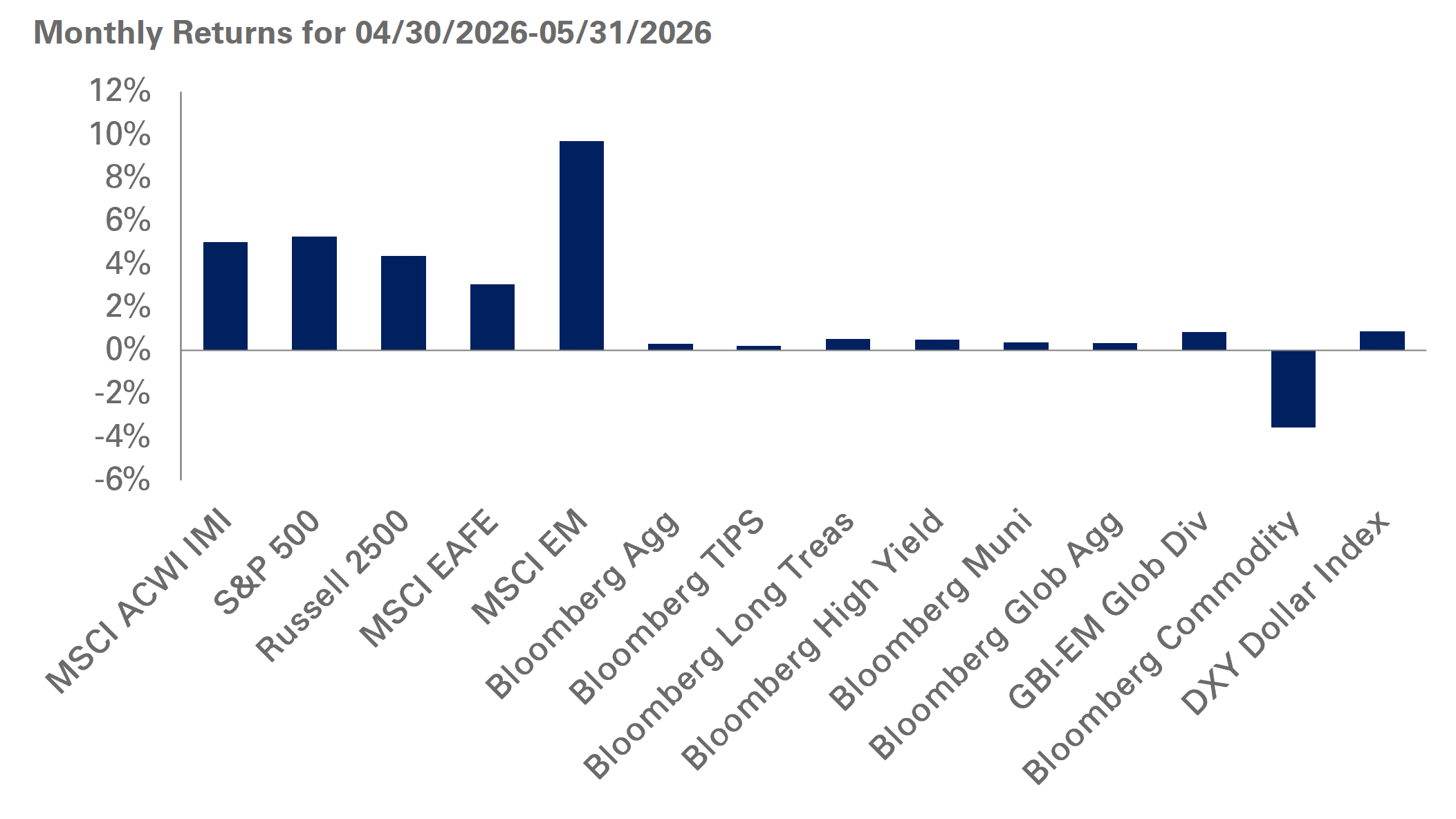

Seasoned investors know that you cannot predict the future of the markets. But smart private wealth managers know that the key to preserving and growing wealth is to anticipate critical trends that are likely to have a lasting impact. Where trends are concerned, 2024 has a lot brewing.

The last few years have seen market tumult and meaningful change in client strategies. What is likely to stick? Here are four compelling trends that the NEPC Private Wealth team is watching carefully for 2024 – and how we are addressing them in conversations with our clients.

1. THE TREND: CONFLICT WILL IMPACT MARKETS

Unfortunately, 2023 was marked by serious geopolitical conflicts, and we do not see that ending soon.

In addition to the humanitarian concerns, these conflicts put pressure on global trade and commodity prices, creating risk and uncertainty for investors.

Developments in Ukraine and the Middle East have already pushed up oil and gas prices. Despite some moderation in late 2023, oil prices remain significantly higher than they were in mid-2020. Persistently high energy prices can act as a tailwind that props inflation up and can force interest rates to stay higher for longer.

THE ADVICE: FOCUS ON REAL ASSETS

We are advising high-net-worth individuals and families to consider adding exposure to real assets – for example, directly in commodities or through private real assets funds. Real assets hold their value better in inflationary environments and may even benefit from rising prices.

2. THE TREND: ARTIFICIAL INTELLIGENCE EXPLODES

Artificial intelligence (AI) has evolved to the point where it is nearly essential in the operational framework of any large company. For example, we at NEPC are exploring the use of AI to help gather and organize the huge amount of portfolio manager data that we receive. But for clients, the larger question is, what is the right positioning to take advantage of AI’s growth?

THE ADVICE: GO BEYOND THE BIG 7

Right now, there is considerable attention being paid to technology’s “big 7” – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. These dominant companies are positioning themselves to benefit from AI’s adoption but, in our view, their valuations are so high that they are prone to volatility at the slightest market blip or earnings disappointment.

Given this, we think it is wise to be cautious about the big 7. We recommend clients trim exposure to mega-cap technology stocks and rebalance their portfolios. They can also look to diversify with global exposure or seek opportunities with AI exposure in the private equity and venture markets.

3. THE TREND: ALTERNATIVES SOLVE PROBLEMS

For several years now, private wealth investors have expanded their use of alternative investments like private equity or debt. The creation of new vehicles, such as venture capital secondary funds, has dramatically expanded the liquidity in these markets, providing private wealth clients with a wide range of products that can be targeted to meet specific risk, liquidity or return profiles. You can even target specific sets of companies, such as global energy transition strategies.

Alternatives have become excellent portfolio management tools, and we anticipate that market to continue to grow dramatically.

THE ADVICE: BE AWARE OF LIQUIDITY AND TAXES

Alternative investments such as private equity can be very additive to a private wealth client’s overall investment strategy, but there are a few minefields that we advise clients to watch out for. For example:

- Liquidity is still a challenge. Distributions from private investments have been slow to be paid out since the market decline of 2022, while funds continue to request ongoing funding from investors via capital calls. This has resulted in reduced cash flow for investors.

Many secondary funds were created to enhance the liquidity of what has traditionally been an illiquid market, but you do not want to be a forced secondary seller. NEPC has instituted “liquidity guardrails” for our clients and we collaborate with them to monitor cash flow. - Taxes need to be considered. Alternatives can be tax-efficient because their returns are typically categorized as long-term capital gains. But that is not the case for every alternative product, and especially for alternative credit strategies. In some cases, publicly-traded municipal bonds have better post-tax returns than private credit; some hedge funds can also provide meager returns after taxes.

4. THE TREND: NEW GENERATION, NEW PERSPECTIVES

Change is coming to the family office. There has recently been a rising tide of retirements from long-established family office founders, paving the way for next generation leaders who may have different investment priorities.

At the same time, we are seeing the next generation becoming more involved in their family’s financial decisions. Younger family members with different experiences and points of view are beginning to exert their influence. In response, family offices are realizing they need to alter their planning.

THE ADVICE: USE TOOLS THAT BRIDGE THE GENERATION GAP

Generational transitions can be disruptive, but there are always ways to bridge the gap. For example, there are many specialized strategies for clients who want to align their capital with their values, or the issues they find important. There are also more traditional approaches to investing that address those same concerns.

If it is the family office itself that is changing, it may be time to reevaluate the roles and resources needed. We often find that ascending family office leaders look to outsource investment decisions, which increasingly is being done through outsourced chief investment officer (OCIO) services. OCIO is an efficient way to allow the family office leadership to manage relationships and financial goals while sourcing high-level investment expertise.

Will these trends impact your portfolio? Please reach out to your NEPC consultant to discuss your plan of action for 2024. We are here for any questions you may have.

Related Insights