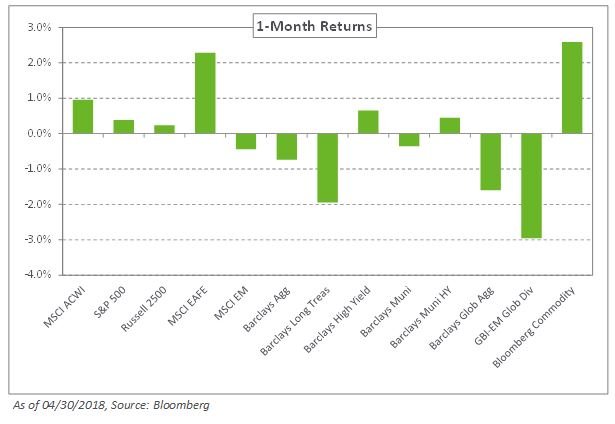

Volatility continued to roil markets in April as trade tensions escalated between the US and China. However, developed market equities still ended the month in the black amid a stronger than expected earnings season; the S&P 500 Index returned 0.4% and the MSCI EAFE Index gained 2.3% for the month.

Within fixed income, the specter of rising inflation weighed on global bond prices with the 10-year Treasury hitting 3% in April – a first since 2014. Meanwhile, the German 10-year Bund rose six basis points to 0.56% and Japanese 10-year sovereign debt increased a basis point to 0.06%. As a result, fixed income was broadly negative for the month with the Barclays US Treasury and Barclays Credit indexes down 0.8% and 0.9%, respectively. Outside the US, the JPM GBI-EM Index declined 3.0% with local currencies weakening relative to the US dollar. In contrast, high-yield spreads narrowed, resulting in a 0.7% return for the Barclays High Yield Index.

Liquid real assets fared well in April with the WTI Crude Oil Spot Index increasing 5.6% as OPEC production cuts and geopolitical instability in some oil-producing regions soaked up excess oil inventories. Additionally, the Alerian MLP Index increased 8.1% for the month as fund flows and improving sentiment helped reverse the prior month’s sharp decline.

Despite the expectation for continued near-term volatility, NEPC’s views remain broadly unchanged as strong growth and fundamentals form the underpinnings of our positive outlook on international and emerging stocks. Furthermore, we encourage the addition of safe-haven fixed-income exposure to mitigate potential market drawdowns and recommend maintaining a diversified risk-balanced portfolio. We also remind investors to evaluate market opportunities, particularly in the event of a more significant short-term dislocation.